Topline: Quarter 3

This quarter was defined by riots in South Africa which pushed the country to the brink of a total shutdown. But as we have done countless times, we bounced back and survived what could have been a catastrophe. Covid maintains its influence on our lives, but as the vaccine rollout continues some semblance of normality has returned with lockdowns being lifted and full stadiums at major sporting events. Globally, we saw some major regulation changes in China that sent markets into a frenzy. There are some headwinds ahead as rising inflation remains a contentious topic with economists and central banks insisting it is transitory of nature. In this review, we look at some of the events that moved markets.

Why the fuss about inflation?

At its very core, inflation points to an increased demand for goods or a decrease in supply which ultimately pushes up prices. If people have money, they tend to buy more goods, thereby pushing up the demand for goods. Alternatively, if the supply of goods is limited, prices may also go up. When this happens central banks generally increase interest rates which ultimately leads to people having less money as their interest payments get bigger, and prices stabilise.

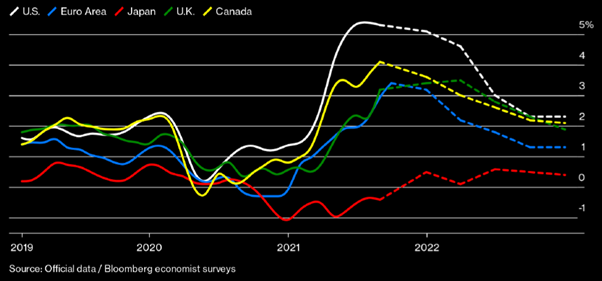

The graph below illustrates current inflation figures and the forecast trends. American inflation is as high as 5% compared to a longer-term average of around 2%. The monetary authorities in America believe inflation at these levels to be merely transitory because of the low base in prices as a result of lockdowns last year this time. They are suggesting that they won’t raise interest rates any time soon. The concern is what if they are wrong?

Markets do not like shocks and if inflation is here to stay it would force these authorities to raise interest rates. This would lead to a shock for equity markets as investors would pour into income assets, and valuations of equities will decline.

Signs we are concerned about are on the supply side of certain goods as well as the labour force in America. On the supply side, for example, there is a massive shortage of microchips which are used in all sorts of products – consequently, fewer goods are produced, yet the demand remains high for those goods. The end result could be higher prices for consumers. On the labour side, you have workers in America taking action in what is dubbed ‘Striketober’. The US is struggling to add back all the jobs lost since Covid struck. The graph below illustrates the current job openings in the US; a number that is more than double the number of unemployed Americans. This could lead to increased wages if companies are desperate to fill positions, which in turn would lead to increased prices for goods (also called inflation).

Whilst this is something that can play out over several years and may be transitory, it is something to keep an eye on as it could have a major impact on markets.

What is China scared of?

Two crises emerged from China this quarter. First, stricter regulations were announced for tech companies across the board with the main focus being on education platforms. This led to a major pull-back of share prices in the tech sector, with Tencent and Naspers feeling the brunt of it close to the South African market. Many analysts suggest that these regulations in the IT sector are long overdue and potentially something that the United States should also be looking at (for social media platforms and the like).

Second, there are growing concerns around the Chinese property market as one of China’s biggest property developers, Evergrande, seem to have major issues in repaying their overdue debt. This begs the question of whether the overall Chinese economy is as healthy as everyone believes – most recently growth numbers also disappointed. With concerns of slowing growth compared to a year ago markets are not taking the news well. Evergrande’s demise would be a bad indicator of property growth in China; we believe the government might step in to avoid a total collapse and that Evergrande might just be too big to fail.

What is happening in South Africa?

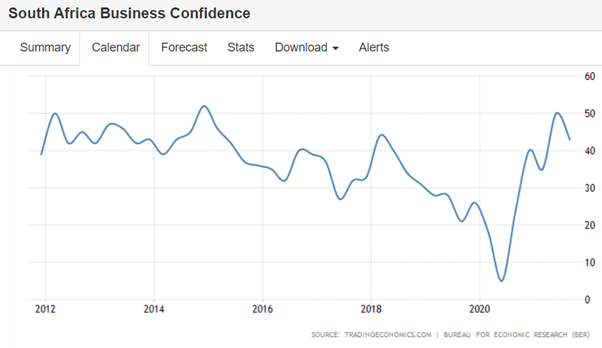

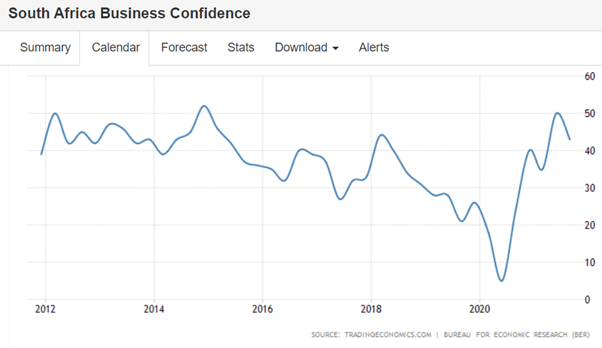

The damage tallied up from the riots in early July, ran into the billions. SASRIA, one of the few state-owned entities in good standing, have pledged to assist companies in the rebuilding and stocking of shops but the government will have to lend additional support. The riots stopped the recovery of business confidence in its tracks as can be seen in the chart below. We must see a recovery in this trend soon if economic growth is to pick up sustainably.

Our vaccine rollout has gained more traction as we are seeing around 1 million doses delivered per week. The UK finally removed South Africa from its red list which is a relief to the tourism industry. Currently, cases are at the lowest levels they have been in 18 months. The biggest concern is around a potential fourth wave for the holiday season, again. Additional concerns around complacency have been highlighted with electioneering in full swing, specifically the mass gatherings every weekend. It remains critical to increase the vaccination rate so that the economy can function at full capacity again.

On 1 November South Africans headed to the polls to vote in the provincial elections. We would turn our attention to the factional battles within the ANC and what good or bad results would mean for President Cyril Ramaphosa. With the ANC having lost ground in the 2016 local elections, it is hard to see how they can turn those battles around with even more municipalities in a dire situation. The RET (Radical Economic Transformation) faction would use poor results against the president to point out his failures. We believe that it is in the country’s best interest for President Ramaphosa to remain in place and continue with the progress towards economic growth and development, however slow. We also hope to see an electorate waking up to alternatives in independent candidates, especially at the local level, so that service delivery can improve at municipalities.

How did Markets react?

Global markets gave back some of the gains made during the year. In South Africa, we saw resources retreat from its stellar run down 3.6%. Naspers & Prosus were also down significantly over the quarter. Shares within the financial sector had a good 3 months up 13%. Property has continued its recovery, up 26% for the year, partly because of the low base. Emerging markets had a tough quarter, down 8% in dollar terms, as signs from China might be pointing towards slowing growth.

What do we do next?

Over the last five years, global equities have provided spectacular returns of over 13% per year, driven primarily by growth in US stocks. We cannot expect these above-average returns to continue indefinitely. The inflation threat may just be what will bring it to a halt, by causing a shock to the system or by causing a protracted period of low growth. Or it may come from a completely different source.

In times of uncertainty, it is easy to try and pivot to take advantage of a certain scenario that is playing out. We would, however, caution against this as things rarely play out the way analysts predict. We have continued to recommend that clients build up an emergency fund or liquidity bucket as we call it. Having access to cash is the best form of defence against market corrections so that your long-term investments can be left untouched.

Benjamin Graham said, “The best way to measure your investing success is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioural discipline that are likely to get you where you want to go.”

For an in-depth review on the quarter you can follow the link to the full review here.