An overview of the fourth quarter

Overall, there was a surprisingly strong performance from most financial markets in the fourth quarter of 2023. Positive sentiment was driven by falling inflation and an unexpectedly dovish rhetoric from central bankers, particularly the US Federal Reserve.

Global equity, bonds, and real estate surged ahead as the market placed its bets on rate cuts for 2024.

Growth in the US continued to surprise to the upside. This provided a goldilocks scenario of simmering inflation whilst job creation remained robust and the consumer relatively healthy.

Oil prices fell significantly over the quarter from just below $100 in late September to below $80 by the end of the year. This drop rather than a price increase, despite the outbreak of war in October between Israel and Hamas, reflects the limited effect of the conflict on the price of the commodity, for now.

Local economic growth continued to be hampered by infrastructure failures. Specifically, ongoing loadshedding – we had 335 days of loadshedding - and Transnet failures. The full impact of Transnet’s failures became more apparent during 2023, with port delays and failing railways placing additional pressure on the road infrastructure.

Despite these impediments, the South African economy likely eked out marginally positive economic growth in 2023. This near-miraculous result is largely due to the continued resilience of the private sector.

What happened in global financial markets?

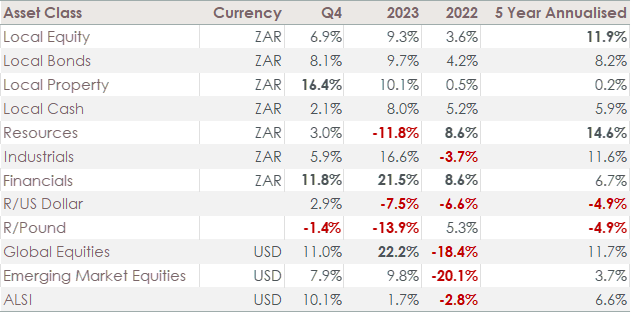

The tables below summarise the asset class movements over the last five calendar years and the last quarter

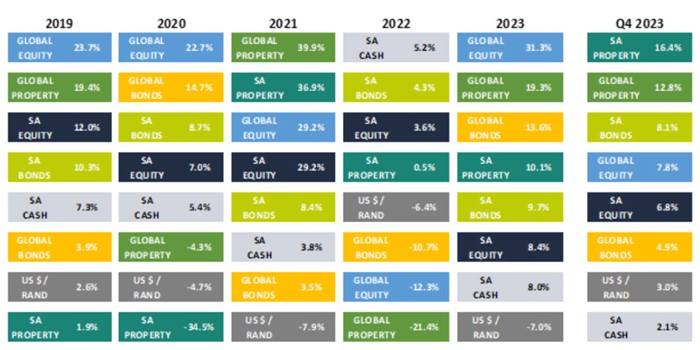

Five Year Asset Class Returns Matrix (in rand terms)

The strong finish in financial markets was due mostly to the last two months of the quarter - the S&P500 provided its 12th-best rolling 2-month return since 1950.

Global equities also performed strongly in the last quarter, with an increase of 11% in USD, having blown off steam in the third quarter. This translated into excellent returns of 22% in USD for the 2023 calendar year. Once again, large-cap US technology companies outperformed and accounted for much of the performance in global equity market indices. Developed markets achieved returns twice that of emerging equities over the year (24% vs 10% in USD). Diversified global equity portfolios with lower exposure to the dominant US tech sector, will have achieved more moderate, but still pleasing growth.

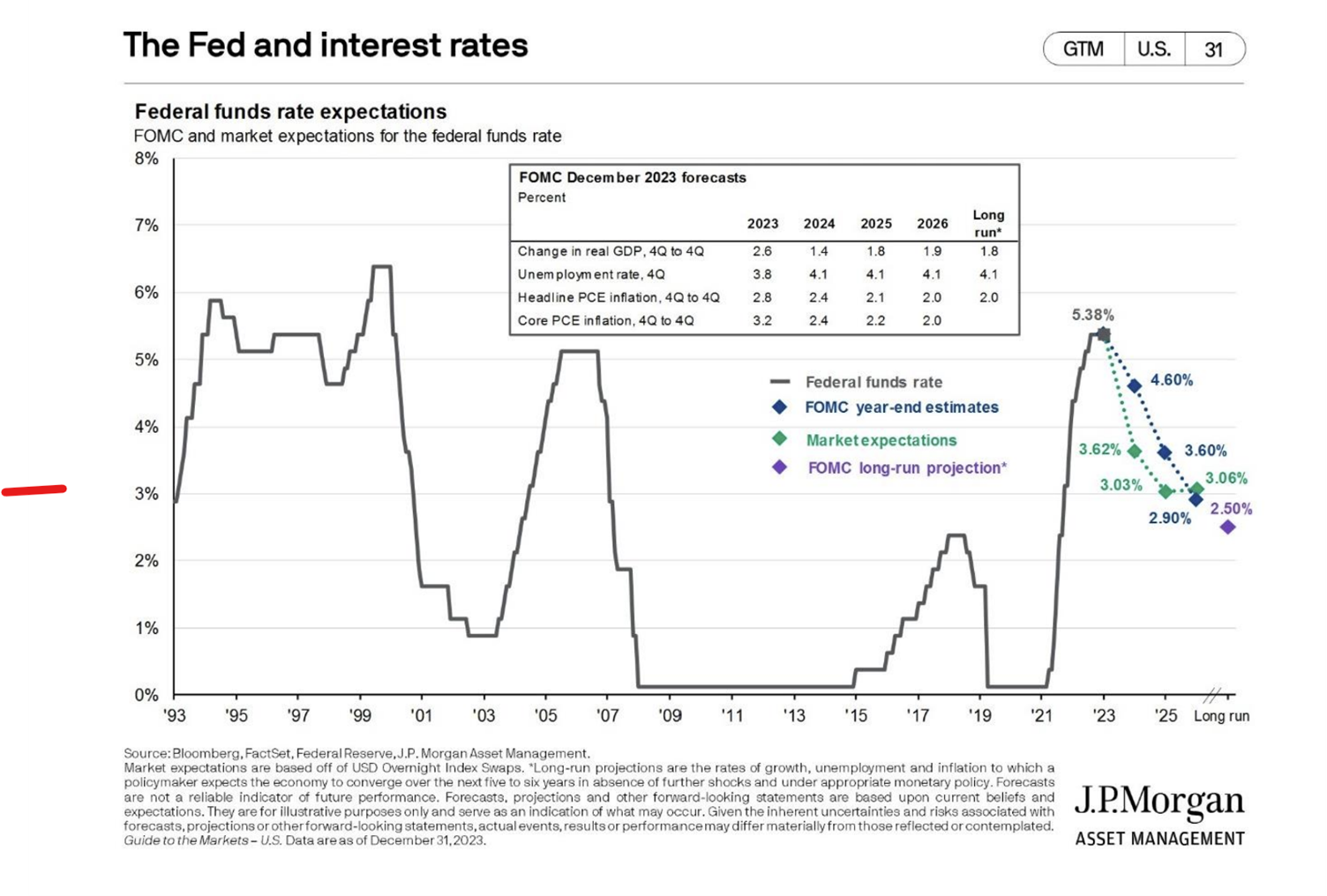

This coincided with the 10-year US Treasury yield falling from a 15-year high in October of just over 5% to under 4% by the end of the quarter. Such a strong move in what is probably the most closely followed instrument in global markets is quite extraordinary and illustrates the extent of macroeconomic uncertainty. However, such volatility in global bond markets has been characteristic of the last few years; Treasury market volatility has increased significantly from the end of 2021 and has remained high since. This is in stark contrast to equity volatility, which has fallen by 2/3rds since 2021.

South African markets benefitted from the improvement in global risk appetite, finishing the year with strong returns in the last quarter. This accounted for much of the total returns for the year.

The South African bond and equity markets, however, suffered significant capital outflows from non-residents throughout the year, with a notable acceleration in December. Full-year outflows now amount to R326.8bn and R154.8bn respectively, according to JSE data. This trend corresponds with a wave of de-listings from the JSE in 2023, with 22 companies no longer on the exchange for various reasons. There are now only 284 listed companies locally, and far fewer investable companies if one applies modest liquidity requirements. This lack of opportunity is a good reason for having healthy global exposure in most portfolios.

The key themes for 2024 are like last year's – interest rates, inflation, and recession. However, elections and geo-political matters may add some spice to financial markets this year.

It remains about interest rates

The most powerful driving factor in the last quarter of 2023 was the Fed’s pivot from a ‘higher for longer’ stance to a more moderate one at their December press conference. Notes state that the “policy rate is likely at, or near, its peak for this tightening cycle”. While the market agrees with the Fed on the general direction of the rates, there is a difference of opinion regarding the timing and speed with which rates will fall - currently, markets are pricing in more aggressive cuts than those implied by the Fed. This difference in opinion will be a source of volatility as we move into 2024.

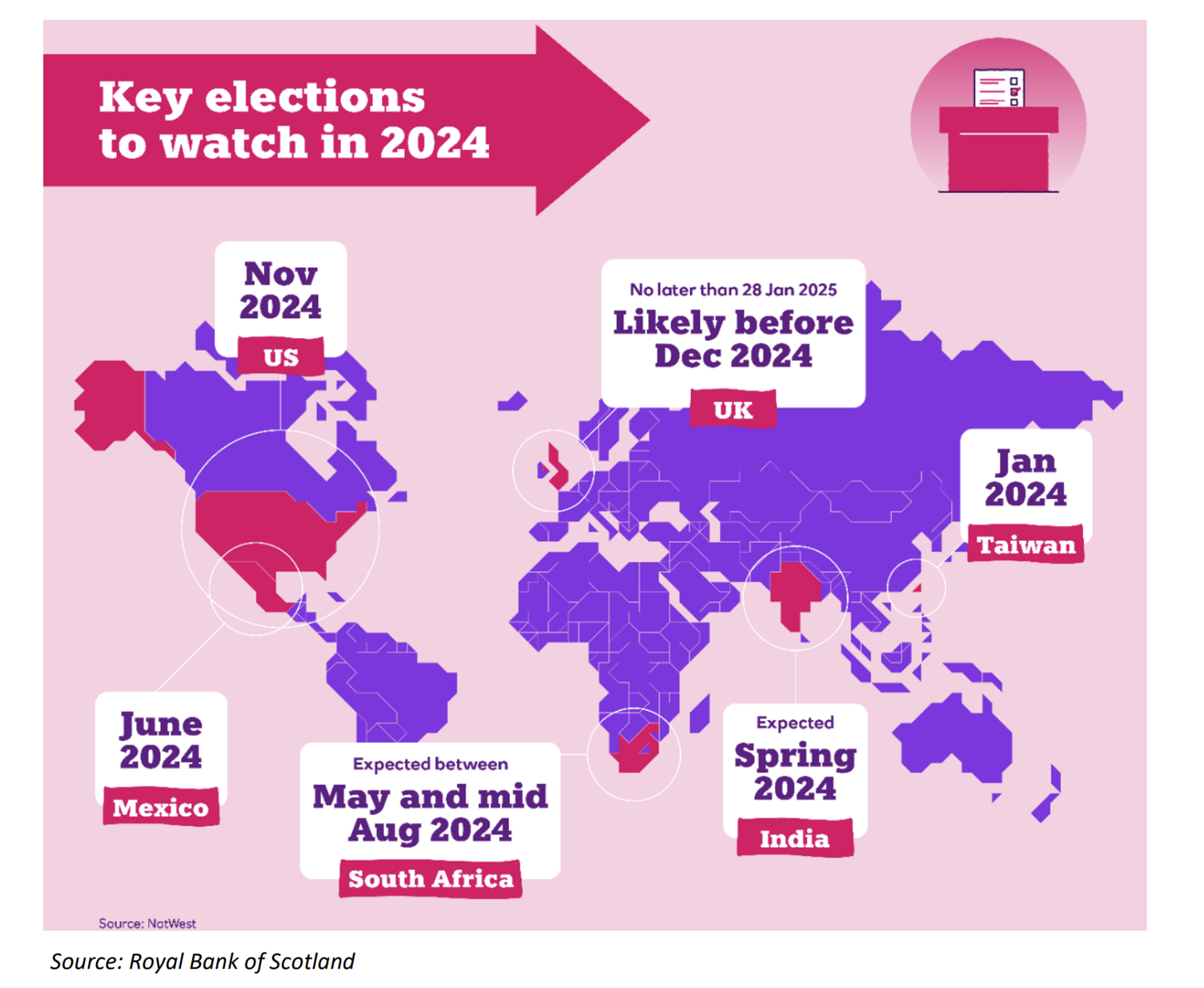

It's a year of elections

More than half the world’s population heads to the election polls this year. Although some outcomes, like Russia and North Korea, are not in doubt, others are more tightly contested and could impact markets.

The US election in November is likely the most significant this year and looks set to be a rerun of the 2020 matchup between Biden and Trump.

Locally, the South African election is significant due to the ANC’s risk of losing its majority. Should that happen, the question of whom they would form a coalition with becomes important, given the probable impact on economic policy. Whilst highly unlikely, an ANC/DA or Action SA coalition could deliver more pro-growth policies. In contrast, an ANC/EFF coalition is likely to shift policy towards an anti-business or anti-capitalist stance.

Although not certain, the most likely outcome is that the ANC will maintain power with an outright majority or a coalition with a small party. This scenario seems to be built into current expectations and would therefore have little impact on financial markets. However, a shift towards the other two scenarios could have a meaningful positive or negative impact on local capital markets.

In geopolitics, the unexpected is not unusual, but it remains important to pay attention to the deeper macroeconomic trends and questions. The interplay between inflation, interest rates, and economic growth carries significant weight.

Inflation needs to come off further

Inflation has continued to fall over the last few months, with falling energy prices (oil and gas) playing a big part. Core inflation - which is headline inflation excluding volatile energy and food prices - has also been decreasing rapidly, but remains above central banks’ targets (2% for the US, UK, and eurozone). The key question for this year is: how quickly will inflation continue to fall and return to target levels? The improved inflation outlook has led markets to shift from expecting further modest interest rate rises from central banks to pricing in fairly aggressive cuts for 2024.

Markets react to changes in expectations; if the anticipated cuts don’t materialise to the expected degree, markets may pull back in response. Japan remains an outlier as it actively tries to stoke inflation after decades of deflation. Its central bank has not yet lifted rates. The success of Japan’s policy normalisation remains important, given the size of its economy.

Will we avoid a global recession?

The question around economic growth is key for this year. The start of 2023 saw many commentators predicting a recession in the US and much of the developed world, mostly due to a sharp increase in interest rates. It didn’t happen, and the US, in particular, saw robust growth. This was fuelled by large government spending and the release of pent-up savings by US consumers over the year. Higher central bank policy rates, which raise borrowing costs for consumers (credit cards and mortgages) and businesses, take time to filter into the wider economy. So, the key question around growth remains: has a slowdown in growth been avoided, or just delayed?

Locally, failing infrastructure will continue to have an impact on economic growth and development. While the electricity situation may improve this year - Eskom is bringing additional generating capacity online and the private sector is rapidly deploying alternative energy - unexpected failures are still likely to occur.

Transnet is likely to get worse before any improvement is seen. Current plans to remedy the situation, including cooperation with the private sector, are too nascent to yield positive results this year.

Conclusion

The good news for investors is that market valuations (the price investors pay for future prospects) are, in most cases, still reasonable, particularly outside the US where they are below their historical averages. Lower prices compensate for a lot of uncertainty and augur well for long-term returns for patient investors.

In South Africa, asset prices are even lower, and bad news is already anticipated. Therefore, even moderately good news could lead to impressive improvements in long-term portfolio values.

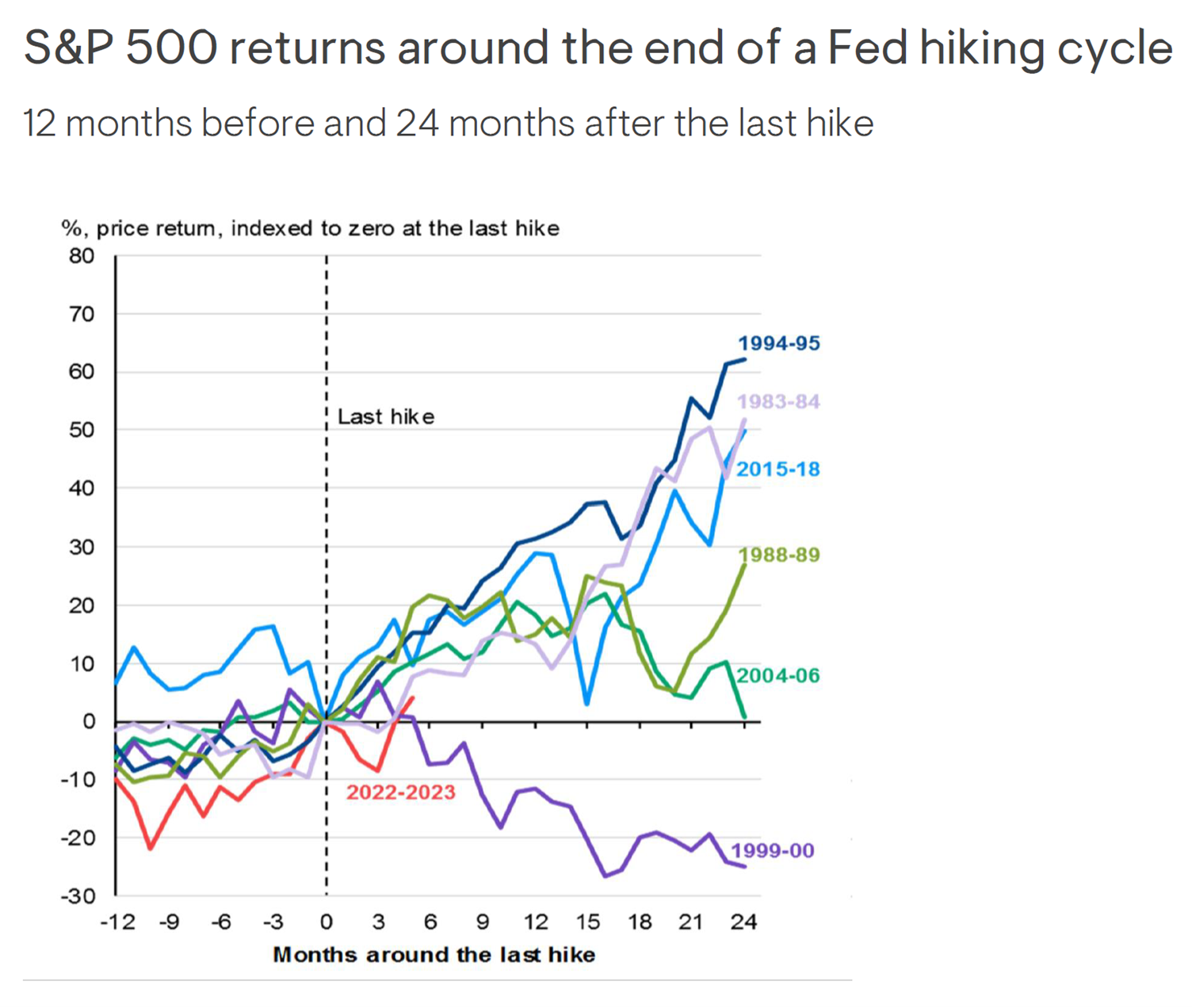

The most important indicator to keep an eye on will be global interest rates, specifically US rates. History has shown that the years following the first interest rate cuts are likely to provide good returns.

In addition, the record level ($8.3tn) in global money market assets could provide a boost for growth assets, such as shares and property, when money market yields start falling.

A year like 2024, with all its potential risk and uncertainty, may tempt us to sit on the sidelines. However, in the words of Benjamin Graham, “Successful investing is about managing risk, not avoiding it.”

As always, we do not try to predict specific outcomes but instead recognise the market uncertainty and remain diversified in our portfolios.

<Foundation Family Wealth is an Authorised Financial Services Provider>