In the final quarter of 2023, global equity markets were buoyed by declining interest rate expectations. In the first quarter of 2024, equity markets delivered impressive returns despite interest rate expectations increasing. Initially, the market reflected about seven anticipated rate cuts for 2024, but this sentiment gradually aligned more closely with the Federal Reserve’s forecasts of three rate cuts of 0.25% each starting in June.

The resilience of economic growth and company profits, especially in the U.S. which had high interest rates, surprised analysts and provided a broadening out of performance across markets. Market growth was less dependent on the so-called ‘Magnificent Seven’ shares, which drove returns last year.

Some cracks have appeared amongst the market darlings, with Tesla and Apple declining in the first quarter due to reduced profit expectations. Concerns remain around the concentration of returns in the top four shares – a situation last seen in the early 1970s.

Source: NinetyOne

We saw all-time highs in Japan, Germany, France and the U.S. amongst others. Bitcoin and gold also surpassed their previous peaks in the first quarter. While such all-time highs should be expected in a growth asset such as equities, it is still exciting news. Defensive assets, such as bonds, fared worse than risky assets. Globally, yields rose over the quarter, which meant that capital values declined.

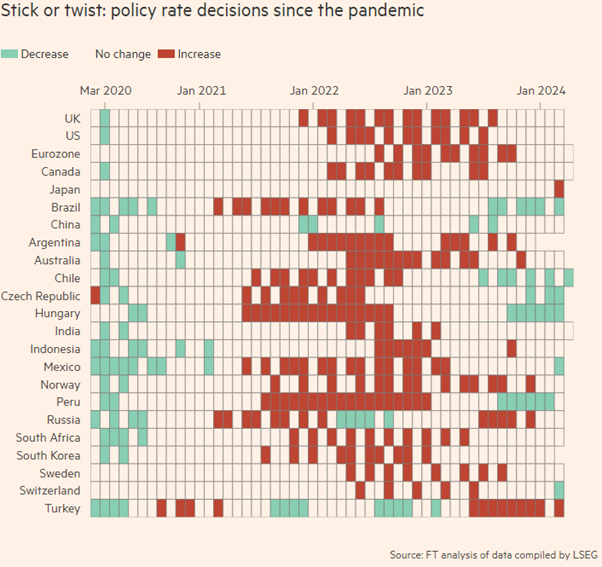

While monetary authorities remain vigilant about inflation and interest rates will remain higher for longer, they are also attempting to avoid recession. This is not an easy task. Currently, the economy seems to be absorbing higher interest rates whilst providing robust economic performance. Authorities are therefore cautious to keep interest rates elevated to avoid inflation resurfacing. However, some countries such as Switzerland, Mexico and Brazil have already started to move interest rates lower.

Oil prices have risen substantially due to constrained supply and conflict in the Middle East. The Russia/Ukraine war and the conflict in Gaza continue with no end in sight, and both have the potential to spread, hitting supply chains and energy exports, which would likely boost inflation.

Source: Portfoliometrix

Global Equity Performance Review

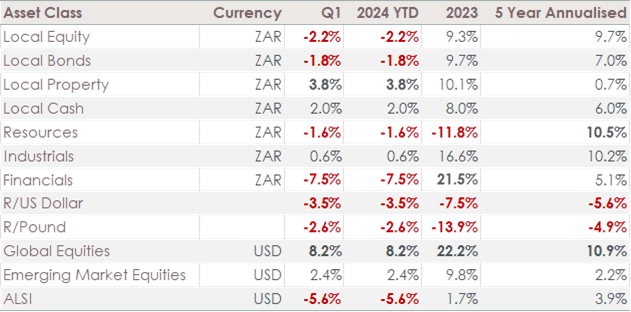

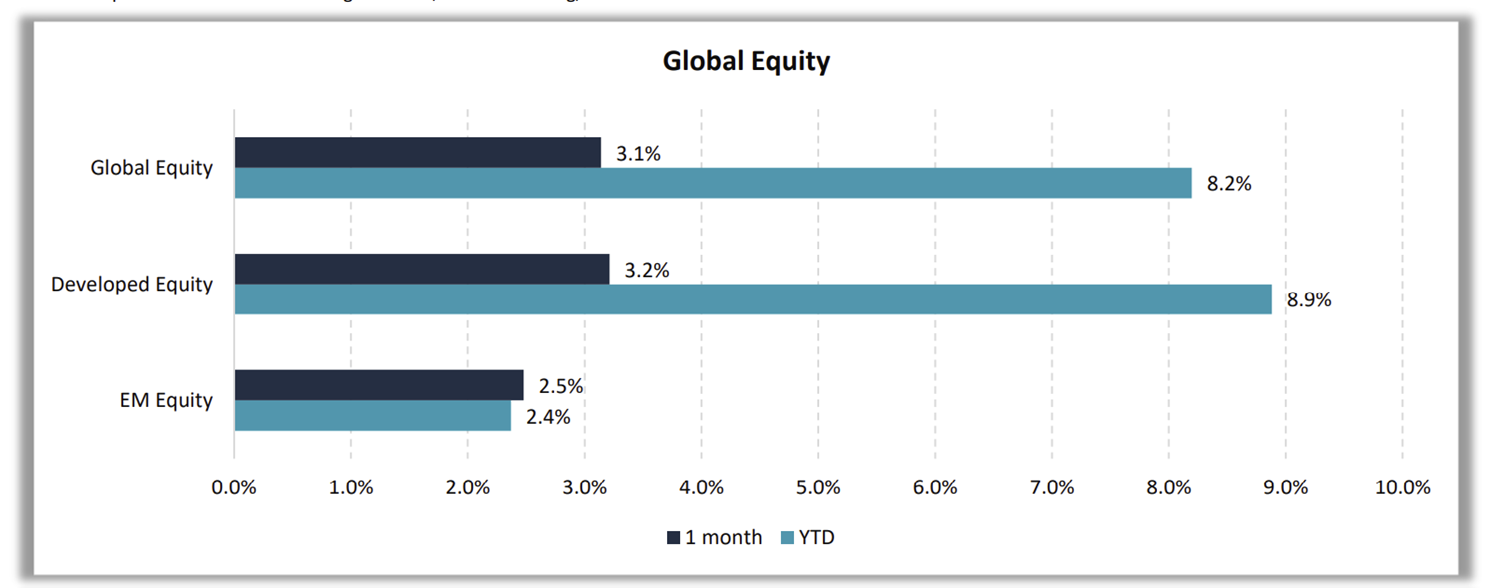

Global equities continued their strong run of performance from the last quarter of last year with another strong quarter at the beginning of 2024. Global equities were up 8.2% in US dollars for the quarter and +20% over 6 months ending March. Developed markets meaningfully outperformed emerging markets over the quarter. This has been the case for over 15 years.

In South Africa, the equity market showed restrained sentiment in contrast to global enthusiasm. The market declined by 2.2% in the first quarter. Investors adopted a cautious stance, likely awaiting the outcome of local elections. This cautious approach is anticipated to persist due to the prevailing political risks and the uncertainty associated with coalition politics in South Africa.

South African sentiment remained depressed

The South African Reserve Bank unanimously decided, at both of its meetings during the quarter, to maintain its key repo rate at 8.25%, marking the fourth and fifth consecutive meetings at 2009-highs, as expected. Policymakers highlighted that, on balance, risks to the inflation outlook were skewed to the upside. Headline inflation accelerated for the second consecutive month, reaching 5.6% in February, up from January's 5.3%, nearing the upper limit of the central bank's target range of 3-6%. Forecasts now indicate that inflation is expected to reach the midpoint of its target range only by the end of 2025, later than previously predicted. It was initially expected to occur by the middle of the year. Positive news over the quarter included the reappointment of Lesetja Kganyago as SARB governor for another five-year term, reinforcing the independence and continuity of the Reserve Bank.

Fiscal developments and market sentiments

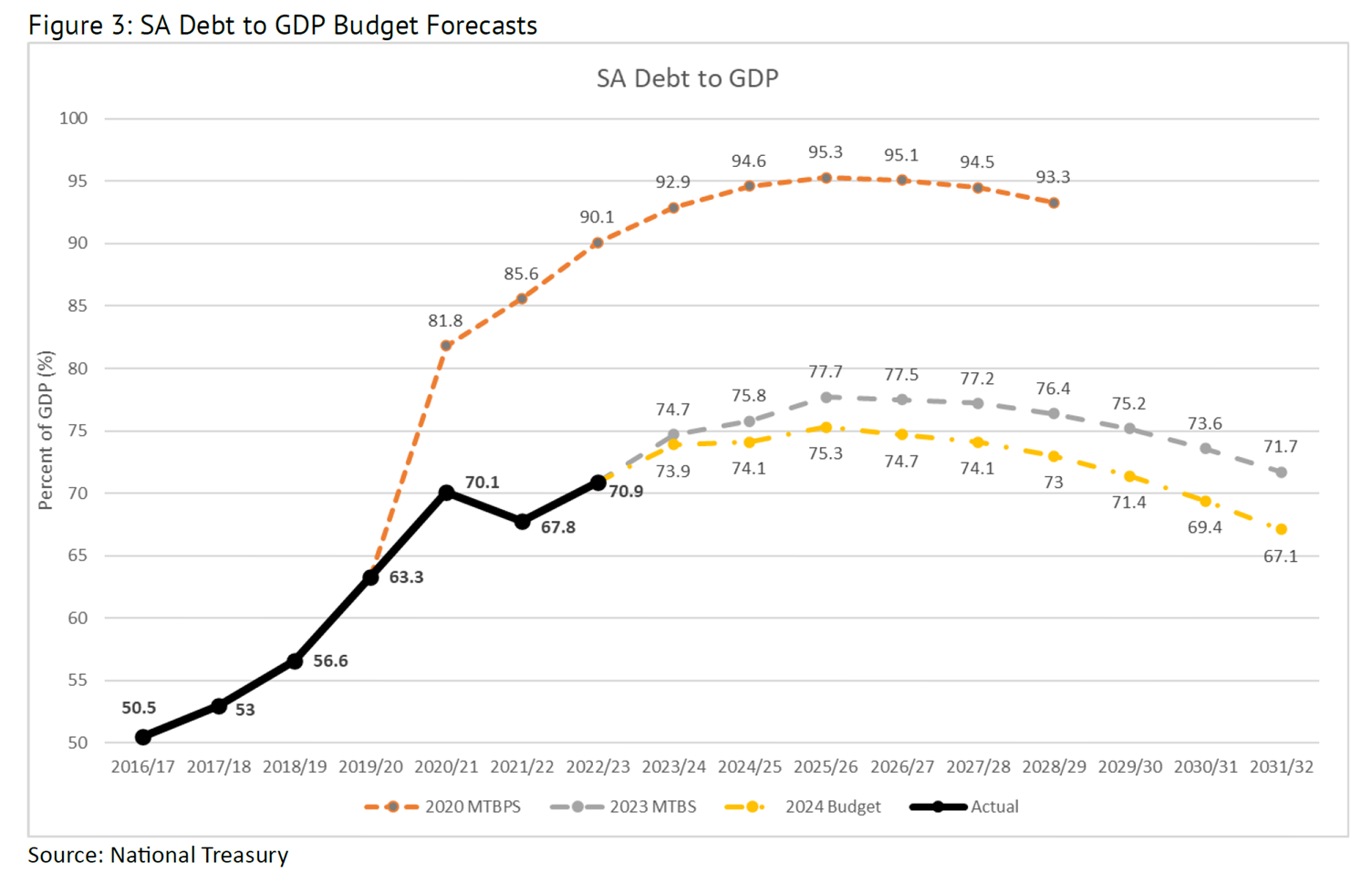

In February, the minister of finance presented a pragmatic budget, projecting a message of tight revenue and tightening expenditure. The budget was mostly positive but does not immediately reverse some of the difficult trends that have emerged over the past few years. The Gold and Foreign Exchange Contingency Reserve Account has been used to reduce the need for fixed-rate issuance (one of the governments most expensive sources of debt), which is a positive development.

The outlook for government debt improved substantially from post-pandemic forecasts. With the vast majority of debt denominated in local currency and a longer average term to maturity, the risk of near-term default is substantially mitigated.

SARS Commissioner Edward Kieswetter, whose term was also extended by the president, announced that the receiver of revenue beat its annual budget by R10bn – an added positive development for the country’s fiscus.

Despite the significant improvements in loadshedding and Transnet operations, SA bonds have had a very difficult period since their rally late last year. This is due to the market following global ‘risk-off’ sentiment and prices in the uncertainty around the general election in May.

For a second month in a row, inflation in South Africa rose marginally in February, with headline inflation moving closer to the upper band of the inflation target with a reading of 5.6% year on year from 5.3% in January. This was considered a surprise by analysts, resulting in expectations that interest rates would remain higher for a longer period in South Africa. After the inflation release, the SARB decided to hold the repo rate steady at 8.25%. After the quarter ended, the March inflation number came in at 5.3%, and although within the target range, the SARB tempered expectations that interest rates might decline this year. They are hoping for inflation expectations to come in line with the midpoint of the 3-6% target range and also want to reduce this range in future.

The May election results may be a watershed event that could produce significant change in our political landscape. The emergence of Jacob Zuma’s uMkhonto weSizwe (MK) Party has substantially changed the likely outcome. Polls indicate that the party could take more than 10% of the national vote, mainly reducing support for the ANC, IFP, and EFF. It could see ANC support falling below 40%. The ANC will almost certainly need a coalition partner after the elections.

Although South Africans have not had a positive experience of coalition governments, the emergence of a different landscape is a positive development. It will likely solidify factions on the left, middle and right of the political spectrum, with the remaining ANC finding itself closer to the moderate middle.

In the meantime, the potential instability creates uncertainty around the future path to resolving the country’s serious structural issues. Despite recent favourable developments within the country, boosting investment confidence and attracting foreign investor interest to the market remains challenging until after the elections. The eventual outcome of these elections holds significant implications for the nation's future trajectory.

The way forward

In a major election year globally, uncertainty is inevitable, and the potential for surprises could move markets materially in either direction. The good news for investors is that plenty of assets still trade at very reasonable valuations, compensating for a lot of this uncertainty. When considering equities, there is better value outside US markets, with the valuation discount even steeper if you look beyond the shares of the biggest equities. Small-cap equities in the UK and Europe, for example, currently trade towards the bottom of their post-financial crisis range and often at a discount to their larger peers whereas they have historically traded at a premium. The same is true for emerging markets and is especially pronounced in South Africa. Nearly all local asset classes show good value, with even mildly optimistic news having the chance to ignite upside potential.

We recognise that market uncertainty is a constant and hence remain diversified in our portfolios. We continue to hold bonds given their attractive yields, but also as insurance against any future recession. We also hold equities for their long-term growth potential, and are cognisant of those areas of the market that are underrepresented and offer opportunities to investors.

The wider diversity in our portfolios has stood us in good stead but may be particularly valuable when out-of-favour markets such as emerging markets and smaller companies return to long-term average returns.

<Foundation Family Wealth is an Authorised Financial Services Provider>