Artificial intelligence continues to dominate the world’s financial markets as a theme. The second quarter saw more gains from the Magnificent Seven, which are beneficiaries of this theme (Tesla, Apple, Amazon, Microsoft, Nvidia, Alphabet, and Meta Platforms). However, other themes featured too: the interest rate outlook, particularly the timing of the first interest rate cuts worldwide, and political developments, specifically around election outcomes, also played a crucial role in determining sentiment.

Short to medium-term risks to real growth and inflation continue, with the range of potential outcomes being particularly wide in the US compared to the euro area.

In South Africa, the absence of load shedding and the establishment of a government of national unity was seen as supportive of financial markets and boosted sentiment.

Global financial markets posted strong results in the quarter ending June 2024, with record highs seen in the US, UK, and South Africa. Towards the end of the quarter, UK and European markets became nervous ahead of national elections in the UK and France.

Market Overview

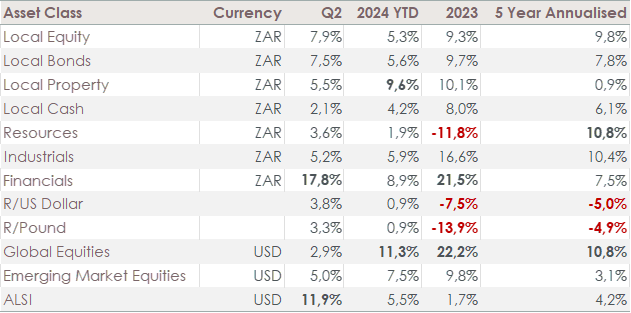

Overall, South African markets reacted positively to the establishment of the GNU. Specifically, markets welcomed the news that Enoch Godongwana has maintained his position as the finance minister. SA equities topped all asset classes with a return of 8% over the quarter, while SA bonds (7,5%) and SA property (5,5%) provided equally impressive returns. These returns mark a re-rating of the prospects of SA investments.

The Rand strengthened by 4% against the US Dollar, resulting in negative returns for global asset classes in ZAR terms. In USD terms, South African equities were the best-performing asset class (11,9%), followed by Emerging Markets (5%).

So-called SA Inc investments did exceptionally well, with smaller companies outperforming large companies (mostly Rand hedge shares) listed on the JSE, while financials (+18%) beat commodity shares (+4%). This came despite a pickup in commodity prices, with platinum and copper increasing by 9% and 8%, respectively.

All eyes are on interest rates.

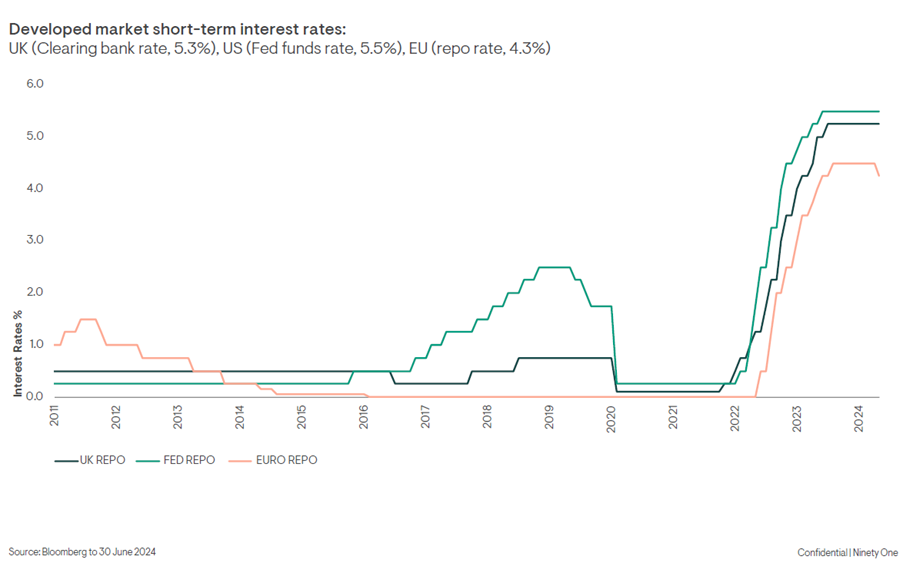

In June, the European Central Bank was the first major central bank to start reducing interest rates despite inflation remaining sticky in the Euro region. Interest rates in the UK and USA remained unchanged, but there are raised expectations for cuts before the end of the year.

The expectation of interest rate cuts has been a driving force behind financial market returns recently. Any indication that cuts may be delayed even further will shock and disappoint global markets.

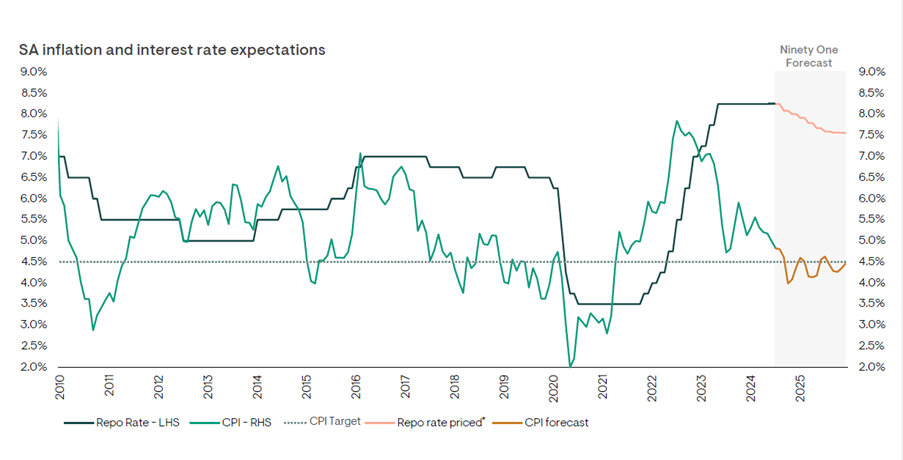

In South Africa, the Reserve Bank has been waiting for inflation to drop convincingly below the mid-range of inflation expectations. The market now anticipates the first interest rate cut at the September meeting and a further cut before the end of the year.

Global inflation appears to be a more permanent feature, fuelled by several factors:

- Increasing geopolitical hostility.

- The rise of nationalism and populism worldwide.

- Growing trade barriers as leaders implement tariffs to protect local manufacturing.

- Onshoring and reshoring of global supply chains (de-globalization).

- Supply chains being re-engineered by political motives rather than commercial motives.

- The increase in government debts and budget deficits in the US during low unemployment.

- The energy transition from fossil fuels to greener technology.

- Potential labour cost increases due to immigration risks.

- Ongoing wars and risks of escalation.

Central banks cannot reduce interest rates, partly because of elevated debt levels. We are seeing more concern over the global debt burden, which has ballooned since the financial crisis and the COVID-19 pandemic. However, contrary to the widespread belief that rising debt loads and excessive government spending signal the decline of America, the US economy and the dollar have grown even more dominant in the global market. Since the COVID-19 pandemic, the US has attracted nearly a third of all international investment, up from approximately 18% pre-pandemic. This dominance has increased despite the prevailing rhetoric advocating for diversification away from the dollar.

Uncertain growth prospects cause volatility.

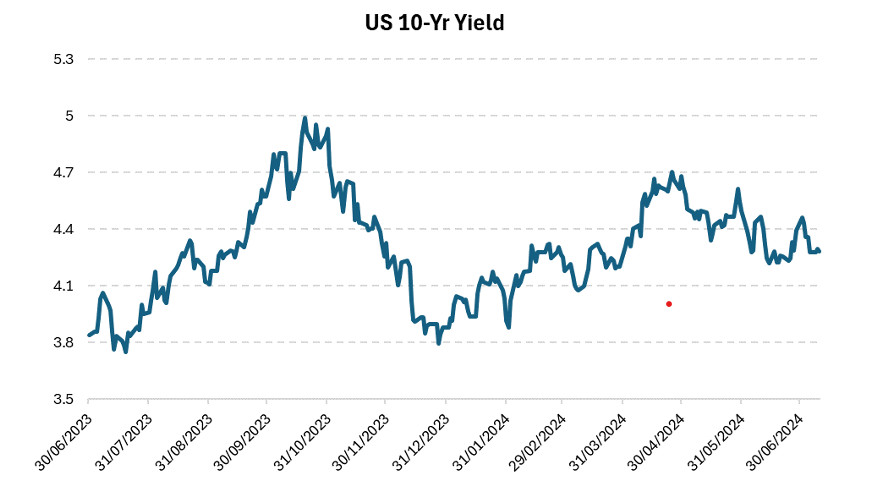

Long-term yields are a valuable indicator of market expectations for economic growth. Examining the US 10-year Treasury yield reveals the volatility in the market’s interpretation and expectations for the future trajectory of the US economy.

Source: Portfoliometrix

Since June last year, the US 10-year yield has fluctuated from under 4% to over 5% and back again, reflecting significant uncertainty about the US economy's future trajectory. This uncertainty is evident in the wide range of analyst forecasts for headline inflation and real GDP in the US by the end of 2024.

Most analysts forecast that economic inflation will fall between 2-4% this year and economic growth will be 1-3%—wide ranges indeed for the world’s most important economy.

Elections will continue to cause uncertainty.

We are halfway through the year of the election, during which more than fifty countries will go to the ballot. Already, we have seen massive change. After the quarter-end, the UK had an enormous swing towards the left, with the Labour Party winning convincingly. Although the right was expected to perform well in the French snap election, a coalition to the left pulled through. In most elections, including India and Mexico, we have seen a shift in electoral support, which will result in policy changes.

Of course, South Africa’s own elections brought an unsurprising shift of support away from the ANC, given their record on delivery. The most surprising element was the rise of former president Jacob Zuma’s MK party. Although the party appears to be disorganised, support for it indicated the discontent amongst disenfranchised population groups.

The GNU, including the DA, IFP and other smaller parties, was formed towards quarter-end. The creation of the GNU represents a shift in our politics to a pragmatic centre focused on service delivery and growth. It also introduced new energy to the cabinet, with representatives from former opposition parties eager to prove themselves. Undoubtedly, the alliances within the GNU will face challenges, and the delivery of promises to voters will be difficult to implement. However, South Africa has an opportunity worthy of attention.

Source: Daily Maverick

Monitoring structural reforms and debt stability

We will monitor progress with structural reforms and debt stability. Operation Vulindlela, the prioritised interventions to fast-track economic reform, provides a roadmap for the reference of new ministers, with a significant level of political support. In this respect, we will look for further cooperation with the private sector, which has already started to bear fruit.

Upcoming US election

The most significant election is yet to come. In November, the USA will go to the polls. President Biden withdrew from the race after a poor showing in a presidential debate with former president Donald Trump and endorsed vice-president Kamala Harris.

This election is critical for future policy direction in the USA. Trump is known to favour tax cuts and growth-orientated short-term policies, which financial markets might enjoy; however, his protectionist economic policies and foreign relations may derail global stability and economic growth in the long term.

A Harris presidency will provide more stability and continuity of economic policy. However, debt stabilisation is unlikely to be a priority in either administration.

The way forward

High debt levels will likely be a central theme over the medium to long term, and most governments are not addressing this problem vigorously enough. However, taking a high conviction stance on the impact of this problem is unwise, given the unusual uncertainty around so many other factors. We, therefore, remain invested in both global and local bond markets.

Even if we were to correctly call the death of the US Dollar, the likely impact on asset class returns is highly unpredictable. Analysts will spend more time deciphering how policy changes due to the changing geopolitical landscape will impact future returns.

Again, our view is to remain invested in well-diversified portfolios. Our clients’ portfolios continue to have a healthy exposure to SA, given that most will retire here. The past quarter has shown how quickly undervalued assets can rerate when sentiment turns positive. Although we do not necessarily believe that SA returns will continue to surprise on the upside, we think it is prudent to remain invested to the extent that our clients’ liabilities are exposed to SA factors.

We look forward to seeing returns broaden from the narrow returns centred around the US tech sector, including healthy returns from emerging markets.

<Foundation Family Wealth is an Authorised Services Provider>