In the 2nd quarter of 2018 US President Donald Trump dominated headlines once again. A meeting with the North Korean president – an attempt to denuclearize the Korean peninsula – eased tensions of a full-scale war, at least for the time being. And a trade war with China imposing tariffs on various goods taking effect in July, reiterated Trumps America First stance.

Locally, we realized just how much work lies ahead if we are to fix our beautiful country. In a tough macroeconomic backdrop, a divided party and looming national elections, President Ramaphosa has a tough job on his hands.

On a positive note, inflation came in lower than expected in the second quarter of 2018. Stronger commodity prices and a weakening rand significantly helped the resource sector on the JSE. The index is up 20% for the quarter – keeping the All Share Index in positive territory.

Ramaphoria dwindling, hard work ahead

South Africans woke up to the stark realization that much is required to turn this ship around as local GDP shrunk by 2.2% in the first quarter of 2018. The decrease was largely due to a drop in agricultural production and is not expected to stay negative for the rest of the year. The Ramaphoria has dwindled and although we have seen some welcome board changes at State Owned Enterprises, management changes at SARS and improved management of the fiscus, the economic impact could take some time to show.

Inflation has come in at lower levels than expected – up 4.4% in May 2018 for the year. Although the inflationary pressure of rising petrol prices and a weakening rand has not come through in the actual figures yet, it is likely to impact the 3rd quarter numbers. Rising inflation could put pressure on the Reserve Bank to raise interest rates.

With elections one year away, Cyril Ramaphosa has little to play with. Populism seems to be the order of the day and the ANC needs to contend with the EFF on these issues. The parliamentary committee will table their report on Land without Compensation in the 3rd quarter. For the ANC this will be the trump card to garner votes back from the EFF. It would suggest that we are in for an interesting ride until then. If Ramaphosa can hang on to an ANC majority victory, or more importantly manage a two-thirds majority – he will be in a much better position to make the changes he sees fit within government. After the elections, (and with some clarity on policies within government) we could see an uptick in capital expenditure.

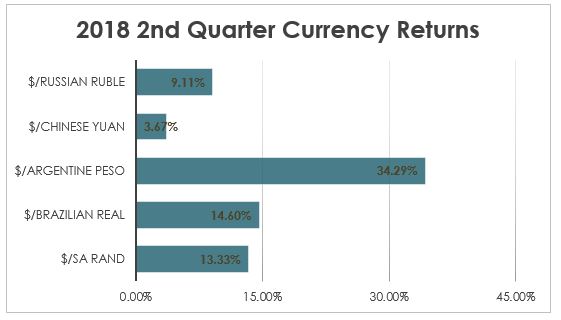

Emerging Markets out of favour

Rising interest rates in the US, uncertainty around trade wars, and higher tariffs on China, have all contributed to a general risk of sentiment that has triggered an exodus of capital out of the developing world. Emerging markets and their currencies took a beating – as shown in the graph below. The MSCI Emerging Markets Index is down 2.8% in dollar terms for 2018.

A tit-for-tat trade war between the US and China has far reaching implications. Our fear is that President Trump might have found his match in China and they might not give in to his bullying tactics and could withstand a trade war in the shorter run. A trade war could lead to higher prices for US consumers which could lead to higher inflation and slowing demand. China could in turn export less products to the US. This could in turn decrease the demand for raw materials and other inputs, which is imported from other developing nations of which South Africa is one. Although South Africans are being impacted by the uncertainty around global trade agreements and aversion to risk, we have not been the worst affected emerging market.

It is difficult to quantify the consequences of such a trade war but it’s easy to see that it is likely to end an era of growing global trade as we know it and to put a damper on global growth.

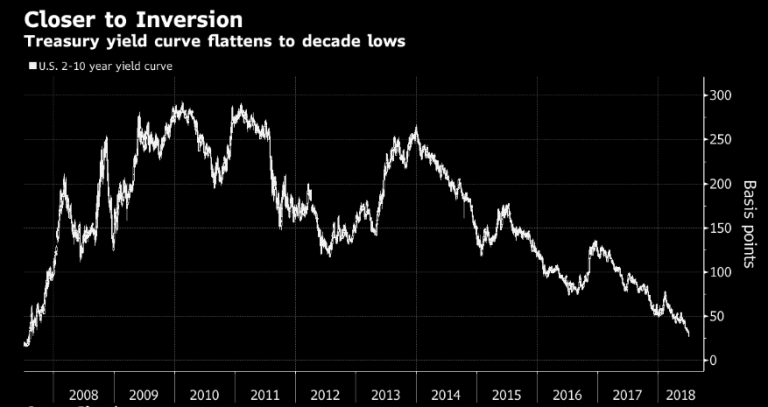

Closer to Inversion – what does it mean for global economic growth?

The graph shows the spread between short-term bonds and longer-term bond yields. In normal circumstances people will want a higher yield for longer-term securities as a reward for the longer period invested. In the current scenario the opposite is happening.

In the United States we are seeing two-year interest yields edging closer to 10-year yields. When the short-term yield surpasses the 10-year yield we have an inverted yield curve. In plain language this is a signal that people are willing to lock in the higher yields for longer periods, as they fear an economic downturn. An inverted yield curve has successfully predicted nine of the last 10 US recessions. Although the exact timeline of a recession cannot be predicted, it is worth keeping an eye on. Analysts believe that we could see the curve invert as soon as the end of 2018 as the Federal Reserve might still hike interest rates twice this year.

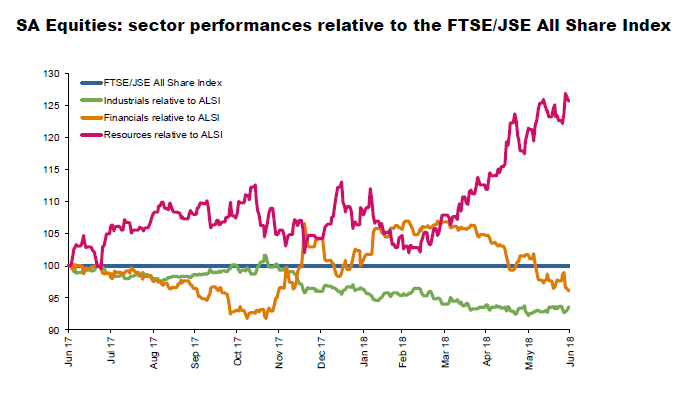

Resource Resurgence

The resource sector has been the only shining light from a domestic equity market perspective throughout 2018. The sector is the only one in positive territory, up 19.6%. The graph below illustrates the performance of various sectors relative to the All Share Index.

A weakening rand and an uptick in commodity prices have been the main drivers of this upward swing. Whether commodity prices can continue to rise will depend on global demand and economic growth. A variety of factors highlighted above could have an impact on the continuos rise of these prices.

The potential risks from the US-China trade has a negative impact on certain commodities specifically used in Chinese production. On the other side oil has benefitted from sanctions and limiting supply from countries such as Iran, Libya and Venezuela. Crude oil is up 13% in dollar terms in the second quarter. Analysts from Deutsche Bank have a year end target set for $80 a barrel.

In Summary

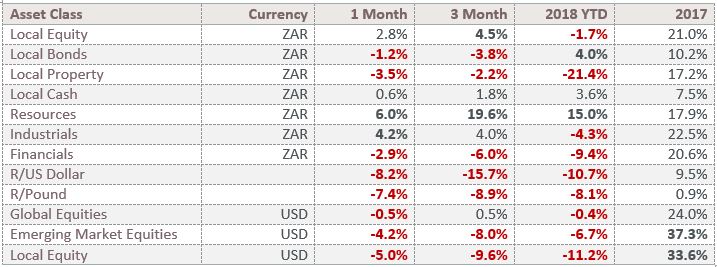

The rand weakened by 16% in the second quarter wiping out all the gains made in 2017 and the first quarter of this year. The property sector continued its negative trend that was triggered when a damning report was released about Resillient’s accounting practices– the sector is now down 21% for the year. Resilient is still down roughly 70% from its best levels despite an independent report showing no evidence of wrongdoing. Local equities bounced back from first quarter losses with Rand hedges coming through strongly in both the industrial and resource sector.

In the past quarter, global news determined the South African investors’ experience. We learnt again, that our fate is determined to some extent by the global stage and not so much around local politics. We also saw though, that these global uncertainties do not necessarily lead to poor returns for South African investors – a weak currency protects local investors because rand hedge shares dominate our market. Short term noise should not detract from longer term goals.

Investors have been nervous since the financial crisis. In the years that followed we have seen one of the longest bull runs in history. Markets have been in positive territory without a 20% drop since 2009.

Attempting to time the end of this bull run is an exercise attempted by many – most of which failed. In fact, some of the best returns, come at the end of a bull market.

“Our stay-put behavior reflects our view that the stock market serves as a relocation center at which money is moved from the active to the patient.”, Warren Buffett

For PortfolioMetrix’s detailed quarterly review, click here.

<Foundation Family Wealth is an Authorised Financial Services Provider>