The Cleanup Crew

<img alt="" class="alignnone wp-image-1485 size-full" loading="lazy" data-cke-saved-src="/DBFile/Image/a82a47b7-7b43-4b7a-90aa-dc8632b83804/01.jpg" src="/DBFile/Image/a82a47b7-7b43-4b7a-90aa-dc8632b83804/01.jpg" srcset="https://www.foundationsa.com/wp-content/uploads/2018/04/01.jpg style=" width:="" 30%;"="">

This Valentines Day former President Jacob Zuma finally made way for Cyril Ramaphosa to be appointed President of South Africa. For this reason South Africans have found renewed optimism. A cabinet resfuffle followed: Nhlanhla Nene was reappointed Finance Minister and Pravin Gordhan was appointed Minister of Public Enterprises.

Within the first few months we have seen some signinficant changes already. Eskom got a new board which were tasked to appoint a new executive. SARS commisioner, Tom Moyane was suspended: a certain schadenfreude moment for Gordhan. Most importantly, the A-Team managed to stave off a ratings downgrade from Moody’s and avoided SA debt being classified as junk. Ramaphosa’s ten point plan to grow the economy, create jobs and stop corruption will certainly boost investor confidence. We are not out of the woods yet but these are some remarkable moves in the first 100 days of office.

However, the National Assembly adopted a motion to allow for land expropriation without compensation. In the very early stages of this debate, it created panic and uncertainty which is never good for investors. A constitutional committee will review Section 25 of the constitution and will need to report back on the issue by 30 August 2018.

Our view is that the highly emotive land issue needs to be addressed. It has become a point of pain for the lack of economic restitution for the majority of South Africans who suffered under Apartheid. Although land is not the only reason for this economic exclusion, it has become the political ball to play. We hope that this committee will bring more certainty to the issue so that we can move forward with even more confidence.

Thuli Madonsela wrote an opinion piece that points out the dangers of creating hope without delivery. You can read the article here.

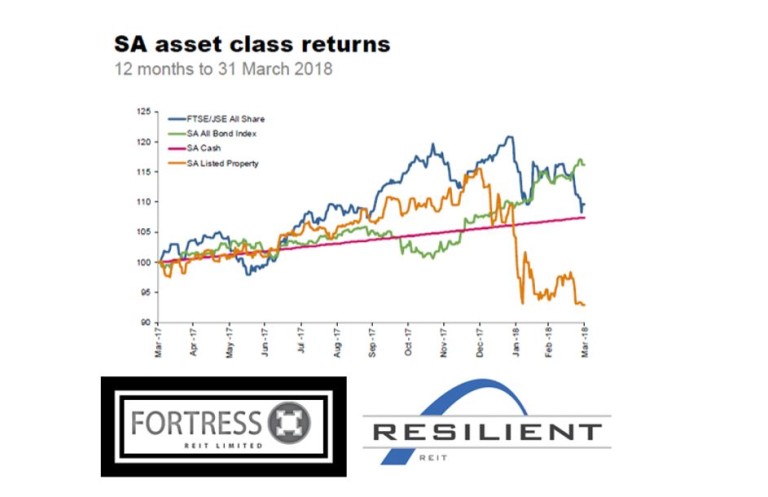

Resilient and distrust

The first quarter of 2018 saw major declines in the property sector with the index down 20%. Rand strength and volatile global markets contributed to the losses, but the main factor once again, was corporate governance. Rumours emerged that Resilient was the next target of Viceroy – the sell side analysts who shot to fame after the Steinhoff report. Asset manager, 36One followed with their report with some damning findings on Resilient and their stable of companies (Fortress, NEPI Rockcastle & Greenbay) and a selloff ensued. 65% was wiped from Resilient’s market cap in the first quarter. The stable made up 40% of the SA Property index at the start of the quarter and the main reason for the major decline.

The concerns raised were as follows:

- Resilient did not consolidate The Siyakha BEE Trust in their financial statements. Income might be overstated due to loans made to the trust and interest payable to Resilient.

- The cross holding of shares where Resilient holds shares in Fortress and vice versa. When share prices rise this creates uplift in the Net Asset Value. The board has subsequently announced an unbundling of these cross holdings.

- The most damning allegation is in terms of price manipulation. Management and related parties allegedly traded the share to prop up the share price. The JSE launched a full-scale investigation, which could take months to solve.

Although an independent investigation has not found any concrete evidence to wrongdoing, the share price remains in negative territory. The JSE and the FSB (newly named Financial Sector Conduct Authority) will release their results in coming months and these will shed more light on the allegations.

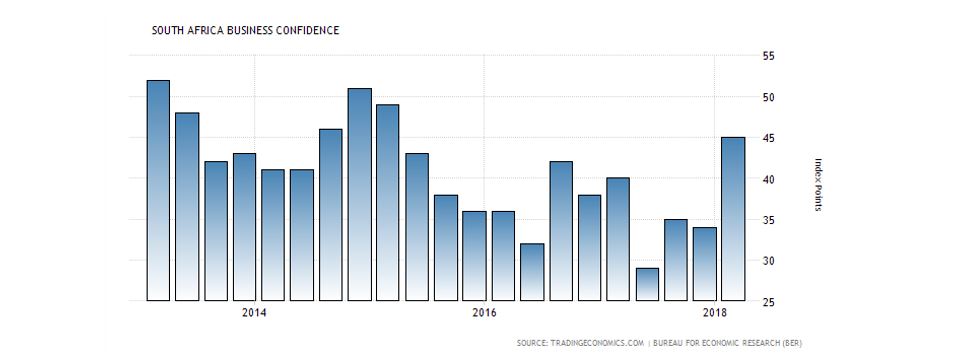

Business Confidence Booming

South African business confidence has risen to the highest level in three years. This recovery comes only months after we saw low levels not seen for 30 years. We have mentioned before that business confidence and consumer confidence creates higher levels of global investment in South Africa.

A clear indication of governments willingness to work with the private sector was the signing of the 27 Independent Power Purchase agreements by energy minister, Jeff Radebe. This represents a potential R60 billion injection by the private sector which could certainly stimulate economic growth in our country.

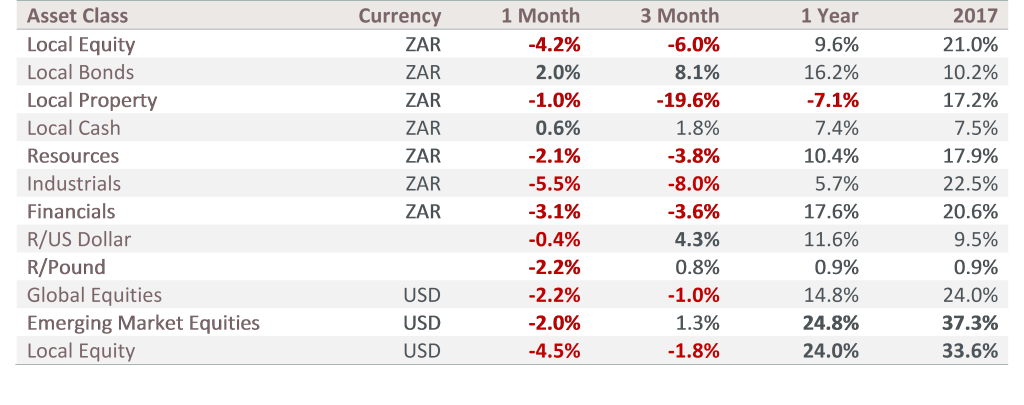

Although the All Share Index is down for 2018, some SA Inc companies (companies with majority of their earnings in SA) have shined:

- Truworths is up 13%

- Foschini Group up 20%

- Mr Price 12%

- Nedbank 14% (to name a few).

We need to bear in mind that the major shares on the JSE have a majority of their earnings in foreign currency and therefore the stronger Rand weighs in on their share price.

Trump and the Trade Wars

As part of Trump’s “America First” rhetoric, the US started the process of imposing tariffs on foreign goods with a 25% tariff on imported steel and aluminum. The current trade deficit with China stands at $375 billion which means that the US imports more from China than it exports. Trump has been vocal about his inclination to erase this deficit. After another set of tariffs, China decided to hit back with tariffs of their own.

The message in the China tariffs were clear: to target Trump’s main supporter base. China imposed sanctions on Soybeans – one of the fastest growing agricultural sectors in the US with a forecast that more land will be dedicated to soybeans than corn in the coming year. Trump won eight of the 10 soybean-producing states in 2016.

As the two biggest economies engage in a tit-for-tat tariff battle, the risk is that this could spill over into a trade war. Trump, in his style of bullying might have met his match with Chinese president, Xi Jinping. This led to increased volatility in global markets and the impact won’t be isolated to the two major economies: it will certainly affect most countries. This story will continue to unfold over the next quarter.

In summary

The first quarter saw a retraction in US stock markets that led to panic that we might head into a bear market. Although global equities were down 1% in the first quarter, it still returned 15% over 12 months, which is well above the long-term average. Locally, property was hardest hit – down 20%, mainly due to the allegations made against Resilient. Local Bonds was the standout performer up 8% off the back of Moody’s decision not to downgrade SA debt.

Markets have not yet reacted as strongly to the positive political changes as perhaps the Rand did. Economic data is hinting that we are moving in the right direction. Inflation was well within the band at 4% that led to a 0.25% drop in local interest rates. Interestingly, Goldman Sachs predicts South Africa to be the big emerging market story of 2018.

With all the political noise detracting from economic fundamentals, it is easy to think we are in a downward spiral. Compared to mid-December 2017, we believe we are on the right track building South Africa up to where it should be.