In his 2024 budget speech presentation, finance minister Enoch Godongwana introduced a new “two-pot” component system that will be implemented from 1 September 2024. The new “two pot” component system relates to retirement funds; however, it was designed with broader financial planning and emergency financial needs in mind.

Under the “two pot” system, people will have more flexibility. You will now be allowed to access some of your retirement savings early if you need to, while preserving a part that you can only touch once you retire. This is meant to help people have better financial security when they retire.

The new system will be implemented across all retirement funds, in both the private and public sector. However, there are exceptions. These include older-generation retirement annuity policies or funds without active members, as well as those in liquidation, beneficiary funds, closed funds, or dormant funds.

Since the initial announcement, significant progress has been made in defining how the new system will operate, what the tax implications will be and how the platform will be administered. There is now considerable clarity on the path forward.

We’ve summarised what you need to know below:

How will it work?

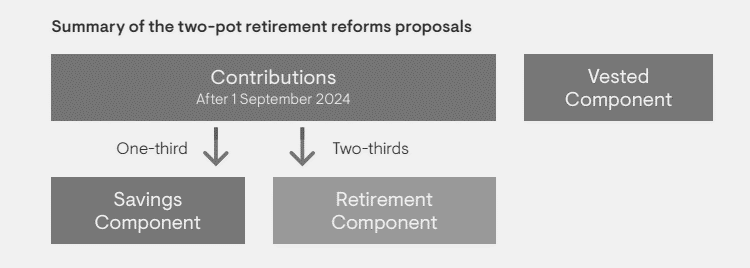

Your retirement fund will now be made up of three components:

The vested component

This component relates to the retirement funds that you already had before 1 September 2024. The old rules (meaning the rules that existed before the enactment of the two-pot system) will continue to apply to this component. For example: at retirement you can take out up to one-third of your retirement savings as a cash lump sum, while the remaining two-thirds must be used to buy an annuity.

You will also be allowed to add to your savings component once the two-pot system is implemented on 1 September 2024. Specifically, you will be able to fund your savings up to 10% of the value that your retirement fund share had on 31 August 2024. This is however subject to a maximum of R30 000 (this is referred to as the seed capital).

The savings component

Once the two-pot system is implemented on 1 September 2024, one-third of your retirement contributions will now be allocated to the savings component. This is the pot you can dip into before you retire, allowing you to withdraw some of your savings if you need to.

You will be limited to one withdrawal per tax year, and the minimum amount you can withdraw is R2 000. This withdrawal will be taxed at your marginal tax rate.

At retirement, you can choose to convert any money left in the savings pot into a single payment (known as a lump sum). This lump sum will be taxed according to the retirement lump sum tax table (where the first R550 000 of your retirement lump sum is tax-free).

The Retirement component

The remaining two-thirds of your retirement savings are strictly for retirement. When you retire, it must be used to buy an annuity, which is a financial product that provides you with regular income for a certain number of years, or life. However, two exceptions will allow you to take the money as a cash lump sum instead of buying an annuity:

- If you cease to be a South African tax resident for 3 continuous years.

- If the total amount in your retirement component is less than the R247 500.

What else will you need to know?

- Your contributions will remain tax deductible at 27.5% of your taxable income, capped at a maximum of R350 000 p.a.

- Withdrawals made before 31 August 2024: any money you withdraw from your retirement savings before this date will be taxed according to the pre-retirement lump sum tax table.

- Pre-retirement withdrawals after 31 August 2024: any money you withdraw from the savings portion that you can access before retirement, will be taxed at your marginal tax rates,

Conclusion

Many retirement fund administrators/platforms will be adapting their systems and processes to the requirements of the two-pot component system. With this change, it is vital to balance this new flexibility with a sound investment strategy.

Although the new two-pot system allows the member to access their funds before retirement, Foundation Family Wealth still firmly believes that retirement investments are long-term investments.

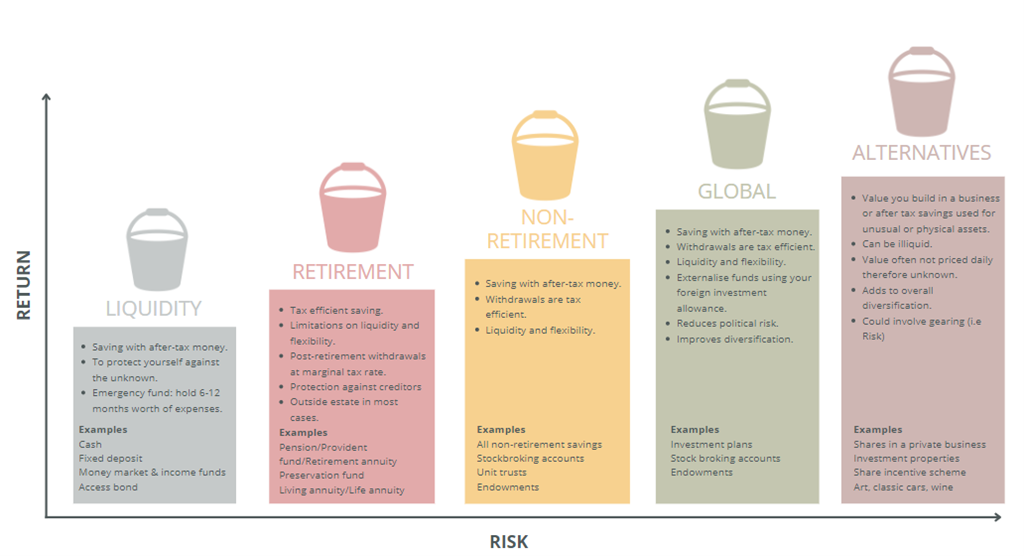

We will continue to use our 5-buckets to wealth approach in which we build your wealth in various buckets over your lifetime. The first bucket is the liquidity bucket has enough funds to cover 6-12 months' worth of expenses in a money market instrument as a form of emergency reserve fund for those rainy days.

For more information and in-depth reading on the two-pot system, please visit the following links:

Allan Gray – “The two-pot chapter”

Ninety One – “Two-pot retirement reform: What members need to know”

Treasury – “Two-pot retirement system”

<Foundation Family Wealth is an Authorised Financial Services Provider>