In the final quarter of 2024, three key global themes stood out:

- Inflation remained a significant concern but showed signs of slowing. Central banks, especially the U.S. Federal Reserve, maintained a cautious approach to interest rates, aiming to curb inflation without derailing economic growth. In general, inflation remained higher than anticipated, leading to fewer expectations for rate cuts in the future.

- Company profits were strong, especially in the U.S., driven by robust economic growth and strong labour markets.

- Political developments impacted sentiment, specifically the election of Trump as US president. In anticipation of tax cuts, market deregulation, and pro-growth policies, financial markets rallied. The US Dollar, in particular, benefited from the post-election sentiment.

However, geopolitical tensions - especially between the U.S. and China - and the ongoing Russia-Ukraine war continued to affect global trade. As markets digested the impact of new tariffs, sanctions, and regional tensions, the positive sentiment waned.

South Africa: Economic and Financial Highlights

- Interest Rates: The South African Reserve bank cut rates by 25 basis points for the second consecutive meeting, bringing the repo rate down to 7.75%.

- Energy Sector: Eskom successfully reconnected the second unit of the Koeberg Nuclear Power Plant to the national grid after a significant refurbishment. This achievement enhances South Africa’s electricity supply, marking nine month of uninterrupted power and boosting business confidence.

- Fiscal Policy: The government has shown continued fiscal discipline, demonstrating restraint in core expenditure (excluding interest expenses).

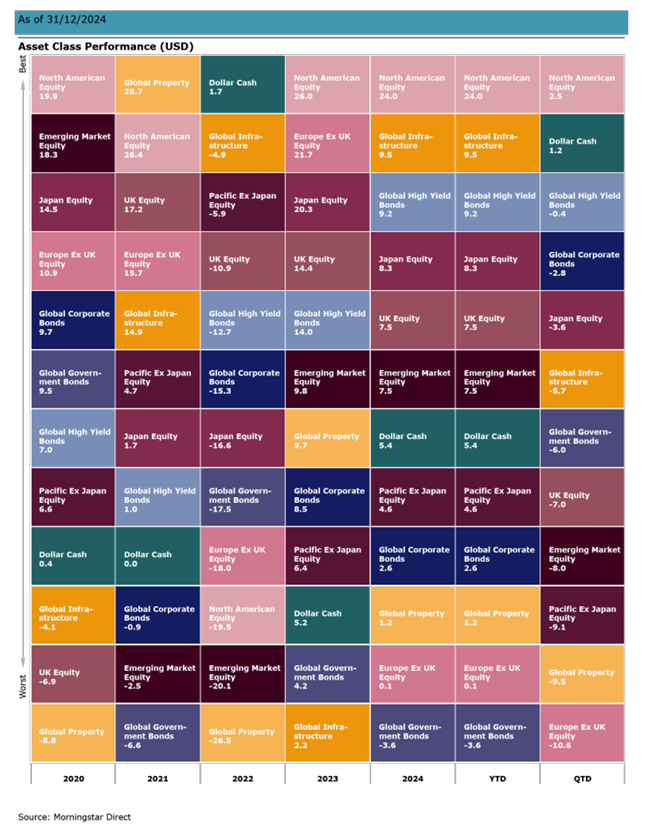

What happened in financial markets?

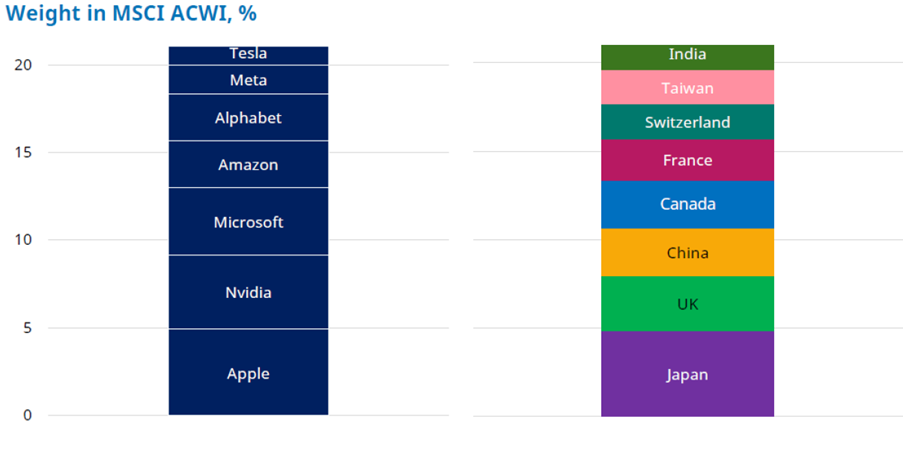

Once again, the North American equity market ended the quarter and year ahead of other asset classes. And again, returns were boosted by the Magnificent Seven. The top seven US companies, including Tesla, Meta, Amazon, and Apple are now worth more than the combined economies of the eight largest nations (excluding the US), as illustrated in the chart below.

Source: Portfoliometrix and Shroders Equity Lens January 2025

This incredible concentration of market value was seen at the Trump inauguration, where many of these company CEOs were present - while numerous global presidents were not invited. While many analysts have long questioned the value placed on these seven shares, this shows how persistent market imbalances can be.

Source: Portfoliometrix

The final quarter of the year showed mixed results across global markets:

- The resilient US economy boosted equity markets, while growth concerns led to a weaker European performance.

- Stubborn inflation reduced expectations for interest rate cuts in 2025, impacting bond markets.

- Japan's equity markets benefitted from a weaker Yen and low interest rates.

- European markets underperformed due to UK budget concerns about potential tariffs on EU exports.

- Emerging markets faced challenges, especially with concerns over US-China trade and a stronger US dollar, which hurt Chinese and Indian markets.

- Global bond markets were volatile, with yields rising and prices falling due to inflation concerns.

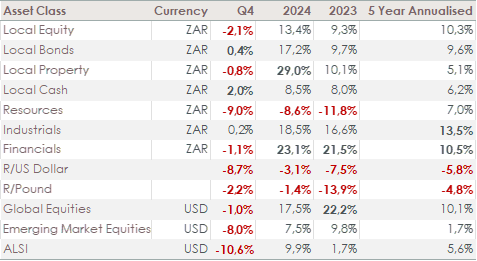

South African Market Performance

While the full-year returns for local property (29.0%), bonds (17.2%), and equities (13.4%) were strong, the final quarter reflected a more subdued environment. Like other emerging markets, South African assets were affected by tariff concerns and deteriorating US relations post-election.

Impact on our client portfolios

Overall, 2024 was a satisfactory year for most investors, with local and global assets contributing to higher-than-expected returns. Most client portfolios achieved returns above 10%, while higher-risk portfolios achieved in excess of 15% over the past year.

Looking forward

Local outlook

While progress has been made to stabilise and improve South Africa’s electricity supply, significant challenges remain in stabilising water supply, ports and railways. In addition, cracks appeared in the government of national unity over land expropriation and national health insurance.

In the short term, inflation is set to remain subdued, hovering near the 3% lower limit of the target range. This gives the South African Reserve Bank room to ease monetary policy a little further. Investor sentiment is improving, with foreign investors returning to South African financial markets.

We will keep an eye on updates from credit rating agencies and efforts to reverse South Africa’s grey-listing status.

Global outlook

Globally, it seems that Trump 2.0 will dominate headlines for a while. Already, the world looks significantly different compared to just a few weeks ago, with a big shift towards an inward-looking, protectionist stance by the world’s most important economy. In effect, we’re seeing Brexit 2.0 in the US, as Trump withdraws from international treaties and looks to slap tariffs on significant trading partners.

Although tariffs have rarely been shown to deliver the desired outcomes, we believe it’s impossible to predict how they will impact financial markets.

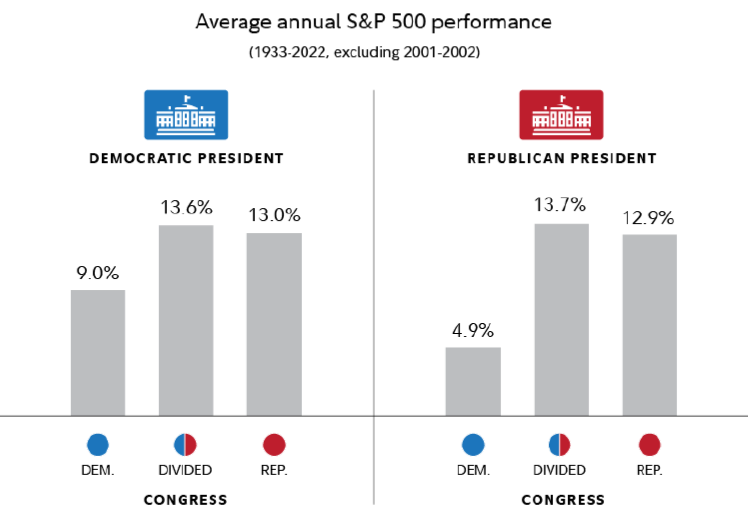

It is tempting to take portfolio positions based on predicted outcomes of the Trump administration’s policy stance. However, from the graph above, we see that politics is not a reliable indicator of what financial markets will deliver.

The year ahead will no doubt be interesting as Trump 2.0 unfolds. However, presidents don’t always get their economic policy changes through a system’s various checks and balances. Beyond the headlines, the underlying financial environment is likely to remain supportive as global interest rates continue to decline.

<Foundation Family Wealth is an Authorised Financial Services Provider>