Using your access bond can be a powerful way to structure an emergency fund, an alternative to a traditional savings account or a money market investment. One that gives you flexibility when you need it, while improving your long-term financial position in the background.

To understand why this works so well, it helps to first understand how mortgage bonds work.

How bonds work

A mortgage bond, or home loan, is a long-term loan from a bank that helps you finance buying, building, or renovating a home. The property you purchase serves as security for the loan, meaning the bank can take it if you do not repay the loan in full.

You receive the loan amount upfront to buy the home and repay it over time, typically 20 to 30 years, through set monthly repayments based on the interest rate charged.

Each monthly repayment is made up of two parts:

- Capital – the amount you originally borrowed.

- Interest – what the bank charges you for lending the money, usually quoted relative to the prime lending rate in South Africa.

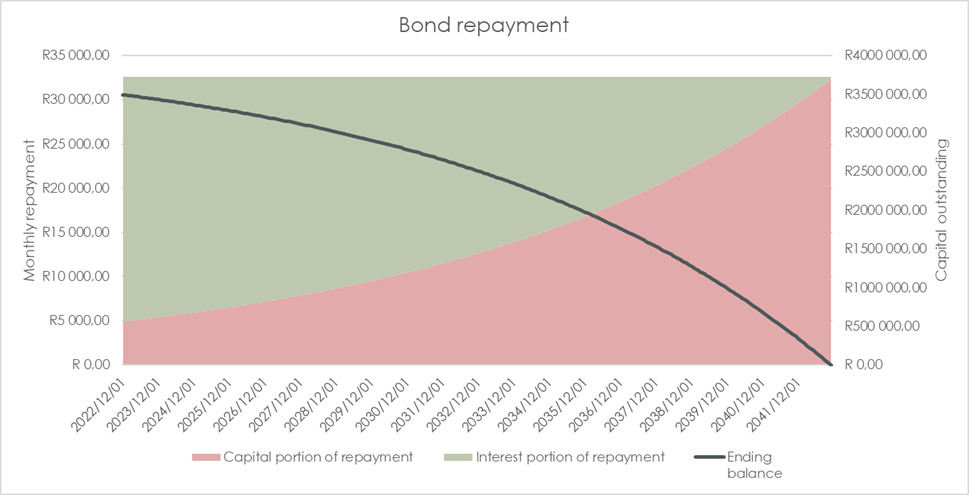

At the beginning of a bond, most repayments cover interest because the outstanding balance is high. As the balance decreases, less interest is charged, allowing more of each payment to reduce the capital amount owed. This automatic shift is called amortisation.

So, while your monthly repayment stays the same over the life of the bond, the split between interest and capital changes. See below:

Graph 1

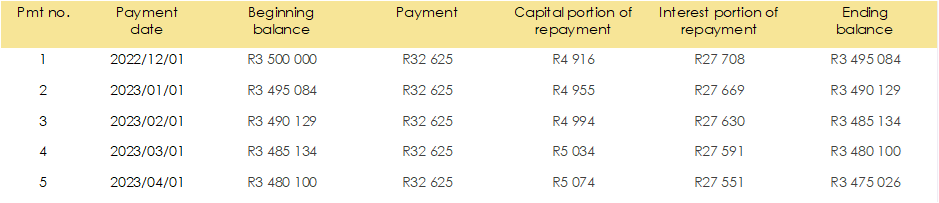

Table 1

Your monthly repayment is the bank's minimum requirement. You can pay extra at any time, which will directly reduce your outstanding balance.

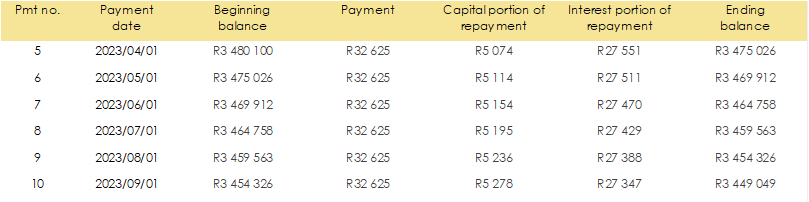

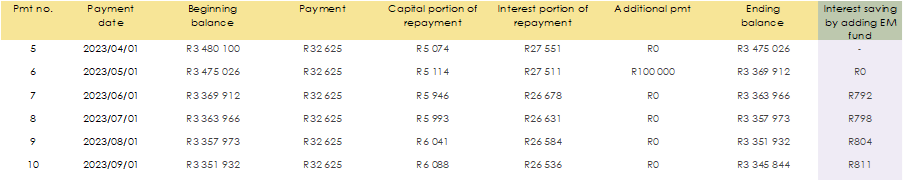

Paying extra reduces outstanding capital, which lowers interest charges. Over time, this means more of each repayment goes toward the capital, helping you pay off your bond faster and save on interest. Compare table 2 and table 3 below.

*Some banks do place limits on extra repayments, so it’s important to confirm any restrictions with your lender.

Table 2

Table 3

What is an access bond?

An access bond is a type of home loan that allows you to withdraw any additional repayments you’ve made over and above the required minimum payments back out of your bond.

In simple terms, if you’ve paid more than required, you can access that money again if you need it.

Why an access bond works well as an emergency fund

Lower interest costs

When your emergency fund sits in your access bond, it is treated as a capital repayment. This reduces the amount you owe on your home loan, lowers the interest charged, and allows more of each monthly repayment to go toward paying off your bond. See table 3 above.

A higher nominal return

Bond interest rates are typically higher than what you’d earn in a savings account or money market investment. A savings account might give you around 5%, and while money market accounts can earn slightly more, those returns aren’t guaranteed and can move up and down.

By comparison, bond rates are often between 8% and 10%. Keeping your emergency fund in your access bond means you’re earning a guaranteed return equal to your bond rate. This makes it a better option to hold short-term cash.

A tax-free benefit

This guaranteed return equal to your bond rate is also tax-free.

You must pay taxes on interest earned in a savings account if your total annual interest income goes over R23 800. At a savings rate of 5%, you will reach this limit with a balance of about R476 000. While this amount may seem high, remember that the tax exemption applies to all interest-earning investments, not just your emergency fund.

For someone paying tax at the highest marginal rate, a 5% savings return can drop to around 2,75% after tax. By contrast, the return earned by reducing your bond remains equal to your full bond rate, as no tax is applied.

Using an access bond provides a significantly better after-tax return while also reducing your taxable interest income, as your emergency fund won’t contribute to your total taxable interest income.

What happens when you access the funds?

When you withdraw money from your access bond, the outstanding loan balance (the capital) increases by the amount withdrawn. In most cases:

- Your monthly repayment remains unchanged

- A greater portion of that repayment goes toward interest rather than capital

- The bond term may extend slightly if the withdrawn amount is not repaid

It’s important to confirm with your bank how repayments are treated after a withdrawal, as policies can differ between lenders.

What to confirm with your bank

Before adding your emergency fund to your bond, it’s important to confirm:

- That your home loan is a true access bond

- How quickly funds can be withdrawn

- Whether any fees or penalties apply

- Whether your monthly repayment changes after a withdrawal

Closing remarks

An access bond only works as an emergency fund if it is used for its intended purpose.

This means only accessing the funds:

- For genuine emergencies, such as medical costs, job loss, or urgent home repairs

- Avoiding withdrawals for lifestyle upgrades or discretionary spending

- Being mindful that repeated withdrawals can delay paying off your bond and increase long-term interest costs

An access bond can effectively serve as an emergency fund when used responsibly. It reduces interest costs, offers flexibility, avoids unnecessary taxes, and provides access when needed, if clear boundaries and discipline are maintained.

Smart strategies only work when they’re applied correctly. At Foundation Family Wealth, we help clients decide whether an access bond emergency fund makes sense for them and how to use it without compromising long-term goals. Sound advice, clear structure, and disciplined planning make all the difference.

<Foundation Family Wealth is an Authorised Financial Services provider>