Look

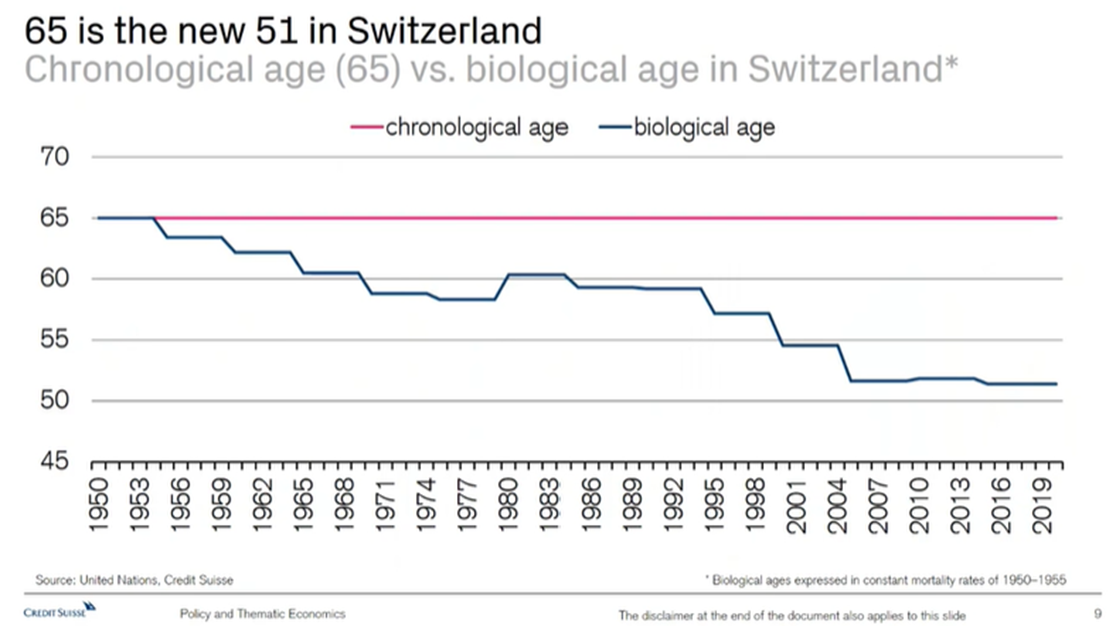

Your chronological age is irreversible and is not influenced by anything other than the date on which you were born. Conversely, your biological age may vary depending on your lifestyle (diet, exercise, sleep, attitude, stress, etc.). Your genetics and life habits determine whether your biological age will be higher or lower than your chronological one. People with a younger biological age compared to their chronological age are at a lower risk of suffering age-related diseases and mortality.

A study in Switzerland showed that the biological age of a group of 65 years olds was now as low as 51. This phenomenon has been on the rise since the 1950s.

Longevity risk is one of the biggest risks to consider when doing financial planning. This is especially true for clients currently in retirement and at risk of running out of money. Using life expectancy tables to see if your money will last is a useful tool financial planner’s often use. However, it may not be appropriate for everyone, as various lifestyle factors and family health history may impact this life expectancy. Each person is unique and therefore individualised planning is necessary. Having a better understanding of a person’s health may help you to plan better and reduce stress and anxiety.

Younger clients may live much longer than today’s retirees. It is crucial for this generation to understand that they should take care of their future-selves by saving enough and starting early. Adopting a healthier lifestyle is a key factor in extending earnings capacity and staying healthier for longer.

We believe that health and wealth converge, and more emphasis should be put on the correlation between your wealth and your health when planning for your life.

Listen

Why is it so difficult for couples to talk about money? Did you know that 78% of couples are more likely to share their dating history rather than their financial history? I believe it’s difficult because of what money represents in our lives. It is deeply personal. For some, it represents freedom and status, but for others, it may represent hardship and pain. For this reason, there could be major misalignments within a partnership that ultimately cause conflict. Financial disagreements or misalignments are the strongest predictors for divorce.

This is one of the most popular short TED talks for 2021. Wendy de la Rosa shares great questions that you and your partner can use to start your money conversation.

Learn

For those that are interested in the topic of longevity and planning for a longer life, I have two thought-provoking books to consider.

The 100-Year Life: Living and Working in an Age of Longevity

The thought of living to 100 and working to age 70 might fill you with dread, but this book helps you to rethink a multi-stage life and extended working career that is wonderful and inspiring.

Lifespan: Why We Age – and Why We Don’t Have To

This is a radical and eye-opening book by Harvard Medical School scientist Dr David A. Sinclair. It delves into experiments in genetic reprogramming and other emerging technologies that may change the way we age forever. For me, this is a slightly unsettling book but still a bold and interesting look into what the future may hold.

Share

Our Foundation community has a wealth of insight and knowledge. With this monthly letter, we would like to launch a poll asking you for your vote. We are looking for hidden gems that we can share amongst ourselves. The idea is to keep it light and fun.

Results from last month’s edition:

What was the best book you read in 2021?

Thank you for sharing your findings. I will be sharing some of your and my best reads in this publication over the next few months.

Click on this link for this month’s poll:

Please share with us your thoughts on looking ahead to 2022. What excites you and what concerns you?

I hope you enjoyed this month’s edition.

May 2022 bring you joy, happiness and good health.

Stay curious,

Elke Zeki, CFP®

Head of financial planning & strategic partner