The first quarter of 2023 kept us on the edge of our seats. Globally, tight monetary conditions are starting to impact the stability of the banking sector. Locally, it was shades of grey. First a grey-listing and then more darkness for the country.

(Another) Banking Crisis Survived for now

March 2023 saw the collapse of Silicon Valley Bank, the 16th biggest bank in America. A few other US banks failed too and as a result, the financial sector lost ground during March.

The forced sale of Credit Suisse to UBS in a deal brokered by the Swiss government followed later in March.

This swift action by the authorities meant that depositors didn’t lose out. However, it raises broader questions about the banking sector’s ability to withstand the economic pain still ahead.

Compared to the 2008 financial crisis, the overall banking system is now much healthier due to increased capital requirements and scrutiny of banks.

Could further rate hikes lead to more pain in the banking sector? US consumers and companies have been used to very low borrowing rates over the last 15 years. However, increased borrowing costs have had an impact on cash flow which could lead to further pressure on the banking sector.

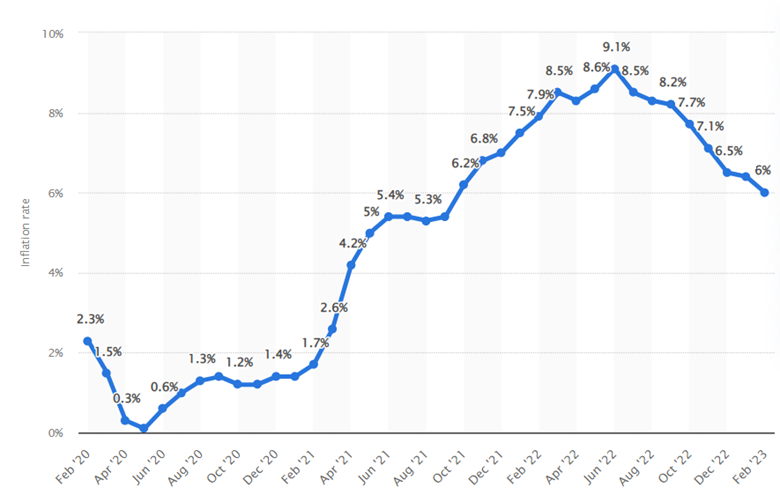

Although inflation is coming down (see the graph below), and rate hikes are starting to slow, the likelihood of recession remains high which could also put additional pressure on the banking sector. Although tightening conditions in the banking sector are a normal feature of the business cycle, asset managers are keeping a close eye on the potential depth of this problem.

US Inflation slowing

Source: Statistica

In South Africa, the banking sector remained sound throughout the quarter. However, the financial sector in South Africa lost 9.4% during March with the news of global banks failing.

With interesting rates remaining high, and the deteriorating economic environment, pressure on bank profits is already anticipated.

The experts’ consensus is that consumer price inflation will fall back within the target range of 3 – 6% during the coming quarter in South Africa; while interest rates are nearing their expected peak and will start to drop off towards the end of 2023. We can look forward to more relaxed credit conditions next year.

Grey listing

Globally, the Financial Action Task Force (FATF) is strengthening its plight against money laundering and terrorist financing as part of its drive against financial crime. A country is placed on the ‘grey list’ if the FATF identifies deficiencies in a country’s ability to counter financial crimes and prosecute those involved.

On 24 February 2023, South Africa was officially grey listed after being under review for some time. From the time SA was initially placed under review in October 2021, 67 areas of concern were addressed by the SA government. However, eight crucial areas still required improvement and consequently, the grey listing was formalised. Money originating from South Africa is now viewed as risky which impacts the country’s reputation and capital flows negatively.

The isolated impact of the grey listing isn’t disastrous; however, this coupled with the country’s poor credit score, lack of investor confidence, and other structural impediments to investments all impact capital flows to the capital-starved economy.

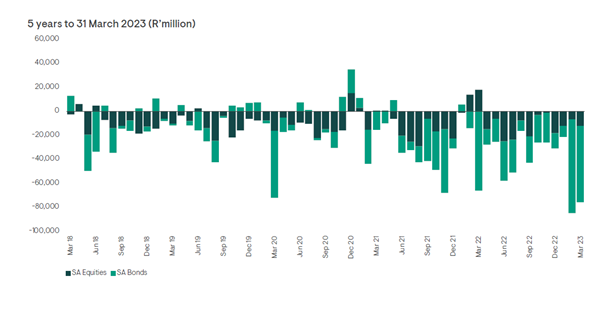

Although significant capital outflows from the local equity and bond market (see the graph below), cannot solely be attributed to the grey listing, it was probably a large factor.

Capital flows to and from the local equity and bond market

Source: NinetyOne Economic and Market Insights March 2023

Finance Minister, Enoch Godongwana, during the budget speech, reaffirmed that the outstanding deficiencies noted by the FATF would be addressed. If done so successfully, as promised, (some of the legislation has subsequently been passed), South Africa could probably be removed from the list in a couple of years.

We are hopeful that a similar story plays out here as it did in Mauritius and Iceland. Fingers crossed.

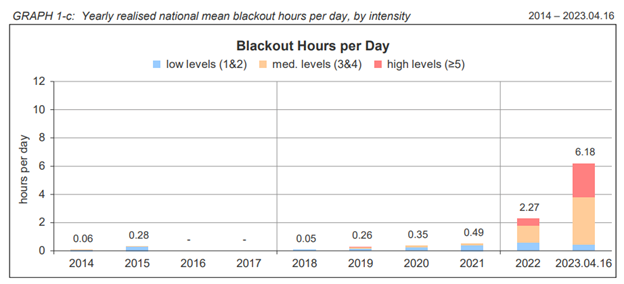

South Africa remains in the dark

The country has experienced load shedding for all but one day of the year so far, totaling 106 days. This is quickly reaching the estimated 250 days expected by the South African Reserve Bank, and more than half the 207 days of load shedding experienced in 2022.

Source: BusinessTech

Electricity Minister, Kgosientsho Ramokgopa, warned that the country will reach stage 10 load shedding this coming winter (when energy needs to escalate) given that the system is already constrained.

It goes without saying that the energy shortage is one of the main reasons for South Africa experiencing low economic growth during the past year. On a year-on-year (yoy) basis, the economy grew by 0.9% in the fourth quarter, significantly lower than the 4.2% growth recorded in the third. Overall, the economy expanded by 2% for the full year of 2022, a notable decrease from the 4.9% achieved in 2021.

However, all is not lost. Over the course of the next two years, meaningful additional capacity will be delivered by alternative energy sources. This alternative energy capacity is largely the result of the government’s interventions to resolve the power crises. This includes loosening its grip on licensing requirements and speeding up licensing for alternative energy production. It is estimated that load shedding may largely become unnecessary towards the end of 2024.

Source: PortfolioMetrix

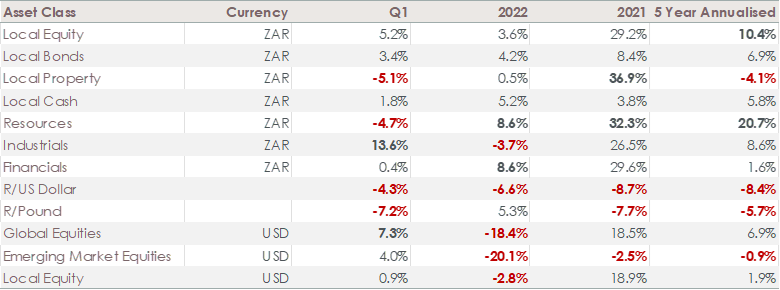

Given the economic and financial turbulence of the first quarter, it may have surprised investors that the JSE was up by 5% during this time. It brought the 3-year growth per year to 24% (off the low base during the pandemic) and the 5-year growth to 10.4% per year. Industrial shares were a stellar performer with the major role-players, Richemont, Prosus, and Naspers, returning 27%, 18%, and 17% respectively over the quarter. Sadly, local property continues to disappoint with a decline of 5% during the past quarter.

Although the JSE significantly outperformed the global equities over the past one and three years, the tables were turned during the last quarter – global equities provided nearly 12% growth in the quarter. A significant portion of this growth was due to Rand’s weakness. Even other emerging markets outperformed the local market.

Global equity returns were driven by stellar returns from the European region. It again highlighted the value of true global diversification.

The Rand weakened by 4.3% against the dollar but was even weaker against the Pound (7.2%) and the Euro (5.5%). This weakness against the Pound and Euro should be seen in the light of relatively lower depreciation against these currencies over the longer term.

These financial market indicators show how much was stacked against South African markets over the past quarter. Political and policy uncertainty, load shedding, and grey listing resulted in capital outflows at a time when exports also weakened relative to imports.

What can we expect from the rest of the year?

The financial news is likely to be dominated by speculation about the balance between economic growth, inflation, and interest rates. Will there be a global recession? When will interest rate hikes end? When will inflation return to ‘normal’? What is the new normal for inflation? In general, a few further interest rate hikes are expected. However, if inflation persists and/or economic output declines, financial markets will be disappointed, and a large correction cannot be discounted.

Globally, there is a cost-of-living crisis. Prices for necessities like food and fuel are at multi-decade highs and salaries have not kept pace. We can therefore continue to expect pressure in the form of strikes, protests, and political upheaval almost everywhere.

In South Africa, severe loadshedding through the winter will, of course, add to political pressure on the ANC and exacerbate already depressed economic conditions.

Although this seems like a bleak picture for the immediate future, we must remember that financial markets always price in expectations. Returns on investments will be driven by whether these expectations are exceeded or disappointed.

Not surprisingly, expectations are low for South African investments, meaning that any good news will likely result in better-than-expected returns. Globally, there are pockets of reasonable return expectations. However, expectations for US shares, which have been the main driver of global returns over the past decade, are potentially still too optimistic and disappointment later this year is not unlikely.

We conclude with a quote from George Soros, “The financial markets generally are unpredictable. So one has to have different scenarios… The idea that you can predict what’s going to happen contradicts my way of looking at the market.”

We agree. Market volatility and different outcomes should be part of our plans.

<Foundation Family Wealth is an Authorised Financial Services provider>