What happened in global markets?

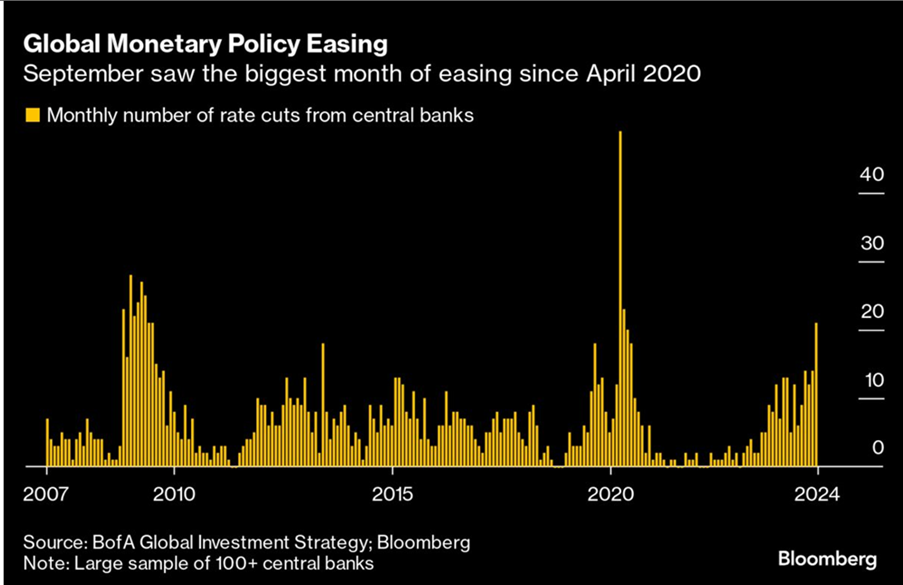

The past quarter witnessed a significant global interest rate reduction, a move that has positively impacted the economy. The US Federal Reserve's decision to cut interest rates by 0.5% towards the end of the quarter was followed by 26 other countries, signalling a collective effort to stabilise the global economy.

China introduced an economic stimulus package to boost its slowing growth rate and support struggling sectors and regions.

The US elections took an unexpected turn on the political front when President Biden withdrew from the race, paving the way for Vice President Kamala Harris to ignite the race.

As a result, markets largely ignored rising tensions in the Middle East, where the ongoing conflict between Israel and Hamas has begun to spill over into neighbouring countries.

What happened in South African markets?

Closer to home, South Africa continues to be surprised by positive developments from the Government of National Unity. Political analysts call this the most favourable trajectory we could have hoped for, and progress is evident in the growing collaboration between the government and private sectors – particularly in efforts to revive ailing infrastructures like Transnet.

Additionally, South Africans finally saw relief with a 0,25% interest rate cut in September.

How did financial markets perform?

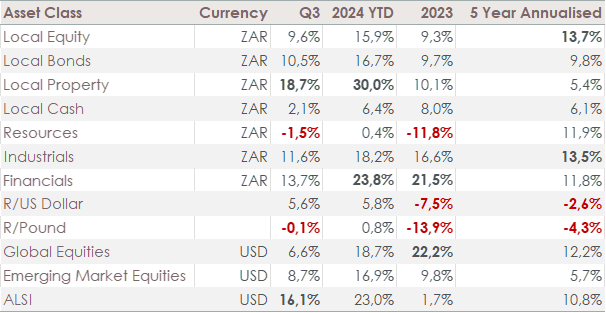

As expectations for further interest rate cuts grew, fears of a global recession started to fade. This led to solid growth across most global asset classes.

Global property topped the charts with an impressive 16,5% growth over the quarter, while the market’s gains broadened beyond the narrow band of US shares that dominated over the past year. Emerging market equities also showed healthy growth, rising by 8,7%.

Property was the standout performer in South Africa, with a remarkable 18.7% growth, followed by bonds (10.5%) and equities (9.6%).

The rand has shown remarkable resilience making it one of the best-performing emerging market currencies. Year-to-date, the rand is up an impressive 5.8% against the dollar. This resilience is driven mainly by positive political sentiment and the Reserve Bank’s conservative stance on rate cuts.

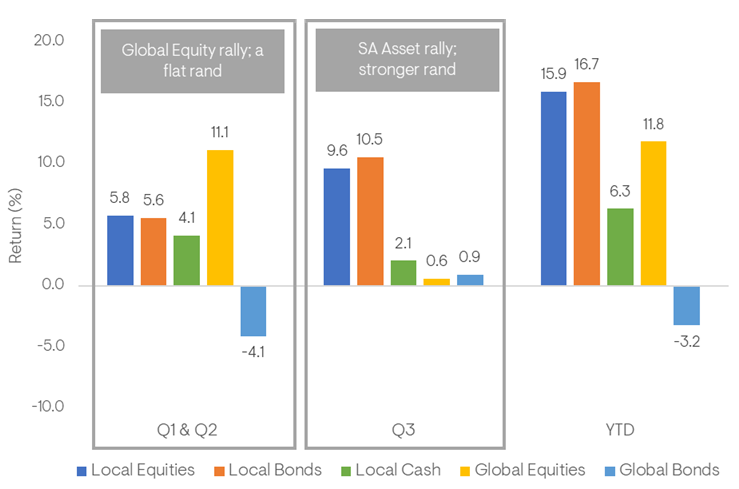

The graph below illustrates the turn in sentiment and broadening of returns after mid-year. Global equities dominated in the year's first half, but local equities and bonds outperformed in the most recent quarter.

Source: Portfoliometrix

How did our portfolios perform?

Earlier this year, most of our clients’ portfolios were rebalanced away from global equities and toward South African equities. This was a difficult decision at the time, especially with the local elections heating up and an uncertain outlook for South Africans. However, we were confident in the long-term potential of local markets, and looking back, this confidence has been rewarded.

Our asset managers’ strategy of managing portfolio risk by adjusting asset allocation - buying local equities at low prices and selling global equities at higher prices – has driven healthy portfolio growth.

Client portfolios have grown by 10-15% year-to-date, with many achieving over 20% growth over the past year.

Although global portfolios have shown healthy returns in USD, the rand's strength has meant that portfolios heavily weighted toward offshore investments have not participated in the recent upswing.

What can we expect from the future?

At this point, global markets are not pricing in a near-term recession. While global economic indicators remain relatively positive, this could change, and there is still the potential for disappointment – particularly given how strongly the markets have rallied.

We caution against expecting current trends to continue indefinitely. The US election, for example, could sour market sentiment, especially if the outcome is disputed or unrest follows. Further, while lower interest rates and a strong economy have offset the negative impact of the Middle East conflicts so far, a sudden rise in oil prices could hurt the markets. The ongoing Russia-Ukraine crisis, which marks its third anniversary early next year, also remains risky. It's important to be aware of these potential risks and consider them when making investment decisions.

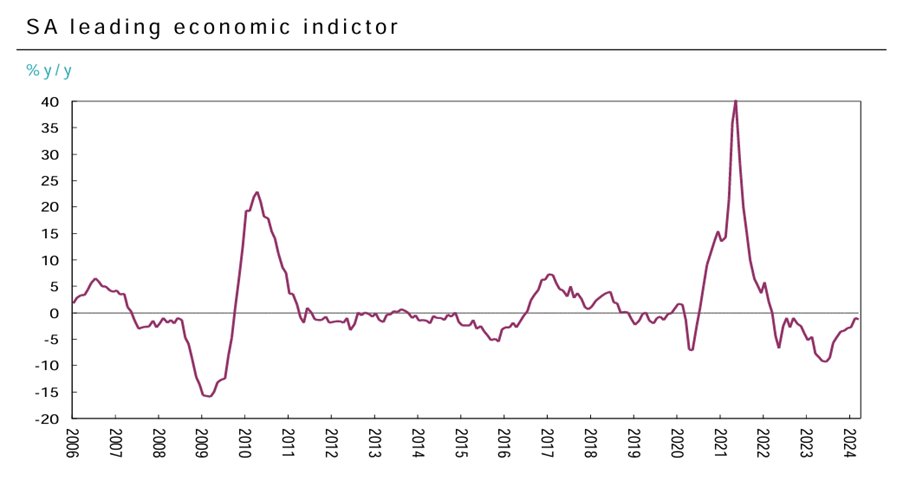

However, early signs of economic improvement are emerging in South Africa, as reflected in leading economic indicators. We also expect further interest rate cuts, and if structural reforms continue to gain momentum, this could significantly improve sentiment and deliver tangible benefits for South Africans.

We remain pleased with the performance of our globally diversified portfolios, which continue to deliver value. Overlooked and undervalued asset classes, like traditional US shares outside the AI boom and pockets of emerging markets, may continue to surprise.

The sudden change in sentiment this past quarter also reinforces the importance of staying invested. Investors who were hesitant and adopted a ‘wait-and-see’ approach have likely missed out on the best gains of this bull market.

Read the full quarterly local report here, and the full quarterly offshore report here.

<Foundation Family Wealth is an Authorised Financial Services Provider>