In the third quarter of 2025, South African markets experienced unexpectedly strong gains due to a growing sense of optimism locally. At the same time, global interest rate cuts indicated a continued easing of monetary policy. Despite ongoing trade tensions, changing positions from central banks, and geopolitical issues, global markets continued their upward trend.

Equity markets advanced, buoyed by resilient corporate earnings and sustained enthusiasm for artificial intelligence (AI).

Emerging markets outperformed developed peers, led by China’s resurgence and renewed interest in cyclical sectors. Notably, Chinese tech firms such as Alibaba, Tencent, and Baidu expanded their AI investment programmes.

In an environment of changing monetary conditions and geopolitical uncertainty, gold has performed exceptionally well, increasing by over 60% year to date. Concerns about significant fiscal deficits in the U.S. and other major economies have enhanced gold's reputation as a hedge against currency devaluation.

The result was a quarter in which both risk and safe-haven assets performed well, a somewhat rare and revealing market dynamic.

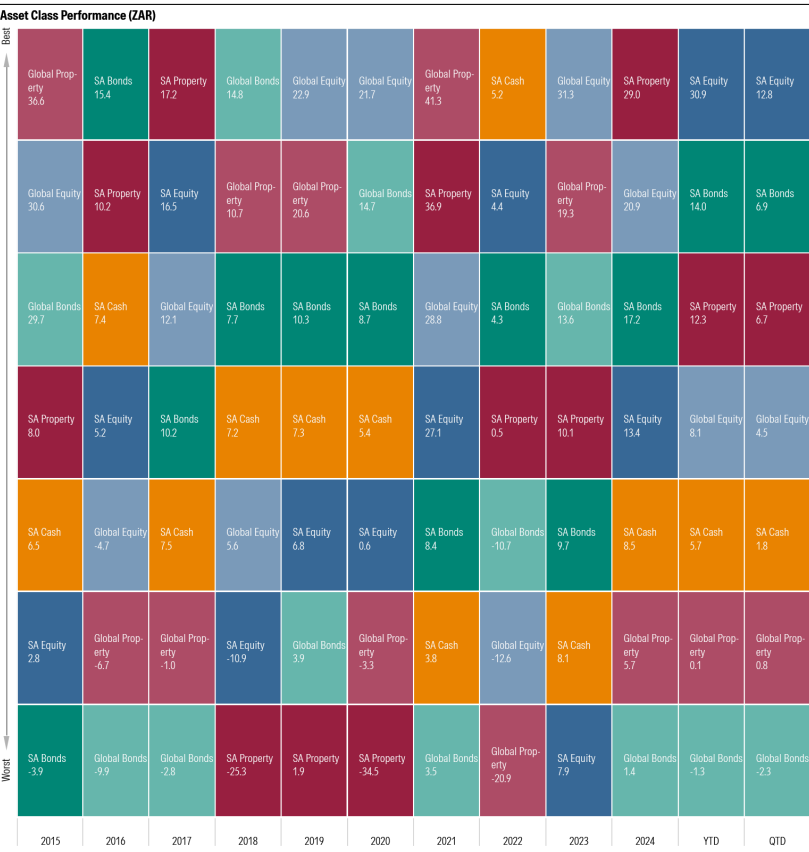

South African equities benefited from these trends, with the asset class topping the pop charts over the past quarter and year-to-date.

Source: PortfolioMetrix.

What happened in South Africa?

Closer to home, South Africa delivered some of the quarter’s most positive surprises. Encouragingly, macroeconomic stability was preserved: inflation remained steady within the target range, and the South African Reserve Bank maintained the repo rate at 7%, citing balanced risks to the inflation outlook.

The policy backdrop was supported by firmer commodity prices, a resilient rand, and improved investor sentiment amid policy stability within the Government of National Unity.

Source: PortfolioMetrix.

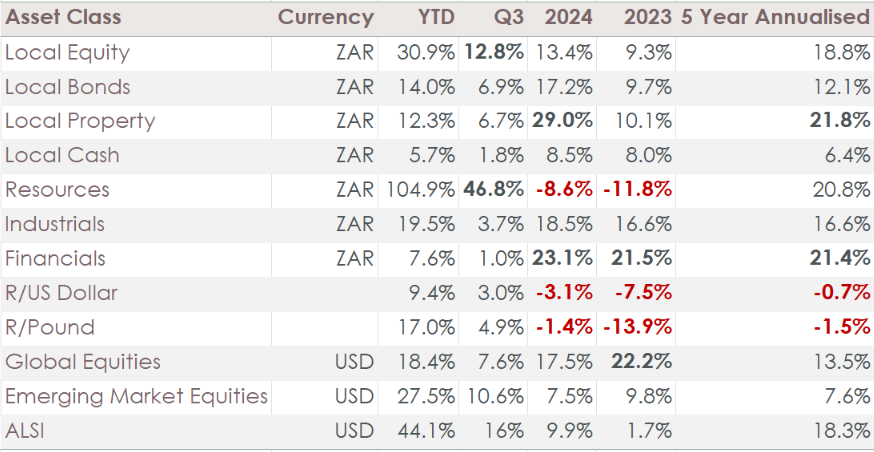

South African equities, bonds, and property markets all posted strong returns. The equity market gained 12,8% in Q3, lifting year-to-date returns to 30,9%. Local bonds followed with 6,9% for the quarter and 14% year-to-date, while local property rose 6,7% in Q3 and 12,3% year-to-date. These strong returns were underpinned by continued strength in commodity shares and increased global risk appetite.

The rand gained 3% against the U.S. dollar during the quarter and is up 9,4% year-to-date, making it one of the better-performing emerging-market currencies. This appreciation was driven by improving fundamentals, high commodity prices, and broad-based dollar weakness. A stronger rand also helped ease inflation by reducing import costs, creating a virtuous cycle of price stability and improved sentiment.

Yet, the composition of equity returns remains concentrated. A handful of stocks – gold and platinum miners, Prosus/Naspers, and British American Tobacco – did most of the heavy lifting. These companies, insulated mainly from domestic economic dynamics, benefited from global tailwinds such as the surge in gold prices and a tech rebound.

Meanwhile, SA Inc. stocks that outperformed tended to do so by gaining share from weaker competitors rather than participating in a broader growth trend. In other words, resilience has come from relative strength, not yet from widespread local economic expansion.

Source: NinetyOne

What moved markets globally?

Monetary policy around the world underwent a significant shift. The U.S. Federal Reserve cut interest rates by 0,5%, and 26 other central banks followed suit during the quarter, marking a coordinated move toward easier monetary policy. Additionally, China introduced new stimulus measures to stabilise its slowing economy. These actions helped alleviate fears of a recession and provided strong support for financial markets.

Asset performance reflected this improved sentiment. Emerging-market equities delivered 10.6%, outpacing developed markets, as investors rotated into undervalued regions.

How did our portfolios perform?

Client portfolios at Foundation experienced significant benefits from these favourable conditions. Earlier this year, we made a challenging yet intentional decision to shift many clients' portfolios from global equities to South African equities. Although this repositioning was counter to prevailing opinions and occurred during a period of local political uncertainty, our commitment to long-term rebalancing has paid off.

The result: most client portfolios have grown by 10-15% year-to-date, with many achieving gains of over 20% over the past 12 months. This outcome validates the importance of strategic allocation and disciplined implementation.

Our globally diversified portfolios achieved strong USD returns, driven by a rally in global equities. However, the strength of the rand diminished these returns when converted back to rand, particularly for portfolios with significant offshore exposure. This highlights the importance of balancing local and global investments. In previous years, a weaker rand boosted offshore allocations, whereas this year, the opposite has occurred.

Because our portfolios are designed with this diversification in mind, clients benefited from both local and global participation.

Another important observation: market leadership, both globally and locally, has been narrow. In the U.S., the rally remained concentrated in a handful of mega-cap tech stocks. In South Africa, a small group of resource and offshore-earning companies drove the majority of index returns.

Such narrow leadership can be fragile. Index returns, while impressive, can mask underlying fragility. Active managers have faced headwinds in such an environment.

Still, the goal of active management remains unchanged: to deliver long-term returns and reduce risk concentration, not to chase short-term index trends.

What can we expect from the future?

While the past quarter’s returns have been exceptional, we caution against extrapolating them into the future. Financial markets remain exposed to significant geopolitical and macroeconomic risks.

The Middle East conflict and the protracted war in Eastern Europe continue to simmer. In the U.S., political uncertainty remains elevated heading into the presidential election.

Despite the existing risks, the overall global environment is generally favourable. The U.S. Federal Reserve's shift toward easing, combined with low inflation, has boosted investor confidence. Additionally, stimulus measures in China and fiscal support in Europe could help promote global growth. However, election-year politics and ongoing trade tensions may create uncertainty and increase market volatility. Valuations in many developed markets are high, and inverted yield curves indicate a need for caution.

In South Africa, there are reasons for cautious optimism. Key indicators are showing signs of improvement. If the Government of National Unity can sustain its reform efforts, public sentiment may continue to improve. Inflation is well-controlled, and further interest rate cuts could be on the horizon. The South African Reserve Bank (SARB) has the flexibility to ease its policy, which would support household spending and increase demand for credit.

Our portfolio strategies continue to provide value, and we believe that certain undervalued and underappreciated asset classes, particularly segments of the U.S. market and emerging markets, could exceed expectations in the long term. This past quarter reaffirmed a timeless principle: staying invested and maintaining a diversified portfolio is essential for long-term success.

Read the full PortfolioMetrix quarterly local report here, and the full quarterly offshore report here.

<Foundation Family Wealth is an Authorised Financial Services Provider>