Global markets: a strong finish to 2025

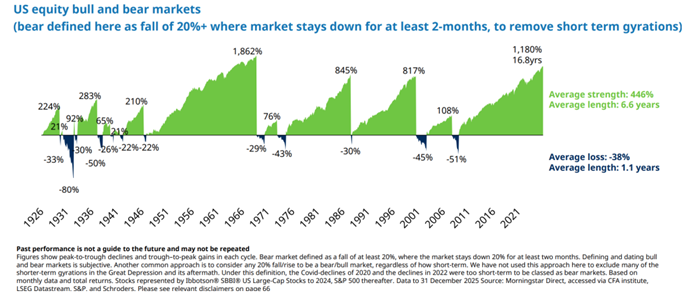

Global markets ended 2025 on a strong note, delivering another year of solid returns despite ongoing economic, political and geopolitical uncertainty. Equity markets were the standout performers offshore, extending a third consecutive year of gains. The current US bull market is now the second longest and strongest since 1926.

Source: Schroders

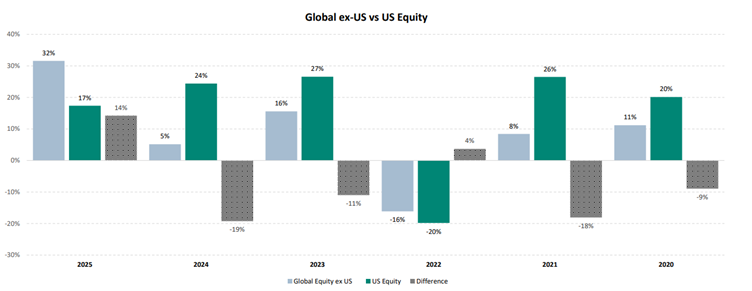

One of the key trends this year was a move away from US-centred outperformance. US equities delivered a solid 18% return, supported by healthy company profits and expectations of lower interest rates. However, other regions performed even better, with developed markets returning 21% to 36% and emerging markets posting gains of 31% to 53%. This rotation was supported by a weaker US dollar, better value-for-money opportunities outside the US, and growing investor selectivity toward highly valued US technology stocks.

Source: PortfolioMetrix.

Artificial intelligence remained an important theme throughout 2025 and continued to support equity markets globally. As the year progressed, however, returns became more concentrated across these companies, and investors grew more selective. Increased competition and questions about the sustainability of future earnings led investors to look beyond the largest technology companies, supporting a broader move into international markets and more reasonably priced stocks.

Gold was one of the standout performers of the year, rising more than 60% in US dollar terms. The metal benefited from persistent geopolitical uncertainty, strong central bank demand, and a weaker US dollar. In contrast, oil prices declined sharply, weighed down by global oversupply and lower demand expectations.

Source: PortfolioMetrix

South Africa: improving confidence, but structural risks remain

South African markets had a fantastic 2025, with most asset classes posting their best returns in over two decades. Equities returned 42,6%, bonds 24,2%, and listed property 30,6%, driven by favourable global conditions, strong precious-metal prices, easing inflation, and improved domestic sentiment.

Over the year, resources were by far the best performing equity sector; however, over the quarter, financials did better, posting a return of 18,4% compared to resources at 10,3%.

Investor confidence was supported by several positive developments. South Africa received a sovereign credit rating upgrade from S&P Global and was removed from the grey list, improving its standing with international investors. Key state-owned enterprises also showed early signs of progress, with Eskom’s latest financial results pointing to a strengthening financial position and Transnet beginning to show tentative signs of recovery. The Reserve Bank’s decision to lower the inflation target should support macroeconomic stability over time, while the Government of National Unity, though fragile, has been viewed as an improvement on previous administrations and has helped bolster market sentiment.

This positive backdrop also supported the Rand, which was among the best-performing emerging market currencies and strengthened by 12,2% against the US dollar over the year.

Despite these encouraging developments, material risks remain. South Africa continues to face long-standing structural challenges, most notably an unemployment rate of around 32%, among the highest in the world. Many municipalities remain financially distressed, resulting in weak or absent service delivery and constraining local economic activity. While market performance and sentiment have improved, the critical challenge is ensuring that this renewed optimism translates into sustained, inclusive economic growth rather than remaining confined to financial markets alone.

How did our portfolios perform?

Locally, returns across medium- to high-risk portfolios ranged from 19% to 21%. Offshore portfolios delivered similar returns in US dollars, ranging from 17% to 20%.

In a year like last, where market returns were driven by a small number of themes, these portfolios typically lag headline indices as they deliberately have less exposure to highly concentrated areas such as gold and artificial intelligence. In addition, portfolios with higher offshore exposure experienced more muted rand returns due to the weaker US dollar.

Looking ahead into 2026

While recent market performance has been strong, it’s important not to assume these returns will continue. Global markets still face geopolitical and economic risks, including ongoing conflicts and political uncertainty, particularly in the US.

That said, the overall environment is more supportive than it has been in recent years. Inflation is easing, interest rates are closer to normal levels, and monetary policy is becoming more accommodative. Alongside continued government spending, this provides a steadier backdrop for growth, even though periods of volatility should still be expected.

Technology, especially developments in artificial intelligence, continues to shape market outcomes. The focus is gradually shifting from optimism and big expectations toward actual earnings delivery. Market concentration remains part of this landscape, as capital continues to flow toward leading companies and dominant themes.

Closer to home, conditions in South Africa are showing signs of improvement. Inflation is well controlled, and there may be scope for further interest rate relief to support economic activity.

Against this backdrop, the focus remains on staying disciplined and well diversified. As always, patience and consistency are key to achieving long-term investment outcomes.

Read the full PortfolioMetrix quarterly local report here, and the full quarterly offshore report here.

<Foundation Family Wealth is an Authorised Financial Services Provider>