I often witness the generosity of older, wealthier parents who wish to leave a legacy for their children. Their hearts full, they want to see the joy their wealth brings while they are still alive. However, their children often feel guilty and are unsure about handling such a financial gift.

An early inheritance is typically a one-time or infrequent financial gift meant to be part of the child's eventual inheritance. Its purpose is to make a substantial impact, such as buying a home, starting a business, or funding education. This differs from ongoing financial assistance for daily needs. Both are forms of wealth transfer, but the intent is different.

In this article, I focus on the first form of wealth transfer.

Giving and receiving money can be joyous and meaningful, yet it can also harm financial well-being and relationships. How should you approach this from a financial planning point of view?

The child’s perspective: Understanding the emotional hurdle

Receiving a substantial financial gift from your parents can be emotionally complex. You may worry about your parents’ financial stability or feel the money is not truly yours; despite knowing you will eventually inherit it.

According to a Merrill Lynch study, many recipients feel guilty and unsure about spending gifted money freely.

Would you feel differently about the money if it came after your parents passed away?

Why use it now?

Using the money while your parent/s are alive, has several advantages:

Shared joy & connection: Share the joy and experiences the money brings, such as a home purchase, funding education, or even a family vacation – they are moments that can be cherished together.

Tim Urban’s popular blog “Wait but Why” had a sobering post called The Tail End, where he noted that by the time you are 18, you’ve already spent 90% of your time with your parents. Assuming they live to 90. If you are lucky enough to still have parents, this means you have between 1% and 10% of all visits left, depending on how old you are. If these financial gifts can help you prioritise these moments, it’s worth it.

Practical support: Address immediate needs and opportunities that might otherwise be postponed or missed.

Financial learning: Reflect on what money means to you, what your personal goals are and how the gift could help you achieve those goals.

Crazy compounding: Imagine saving for retirement instead of paying for a home loan. You could end with almost 4 times more retirement savings due to the powerful compounding effect – which then also helps set you up to create generational wealth.

The parents’ perspective: Protecting your financial future

I believe that the biggest gift you can give your children is your own financial independence. For many South Africans this is not possible. Most parents spend their working lives supporting their children and once retired, the tables turn, and the children start taking care of the elders.

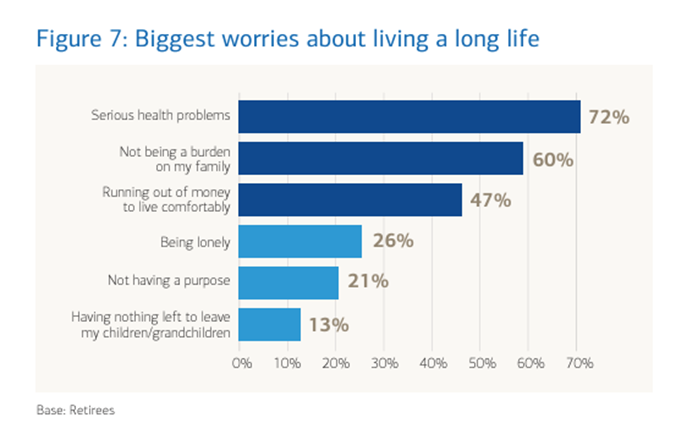

Planning for your retirement should therefore be a priority. Merrill Lynch’s research shows that 60% of retirees worry about being a burden or running out of money to live comfortably. You can consider financial gifts to your adult children only if your financial freedom is secure.

Why give it now?

Shared joy: Experience the joy and gratitude of seeing your support positively impact your children’s lives, strengthening relationships and connection – key in your old age.

Mentoring: Guide your children in managing money responsibly, contributing to their financial stability and growth.

Happiness: It aligns with many people's values and sense of purpose. It can provide meaning and fulfilment in your life and enrich your emotional and psychological state.

Estate planning: For larger estates, donating funds to your children can reduce death taxes as donations tax (20%) is lower than the top bracket of estate duty (25%).

Responsible Stewardship

The key to successful gifting is responsible stewardship. Recipients often feel a heavy responsibility to honour their parents hard-earned money. So, what does responsible stewardship look like?

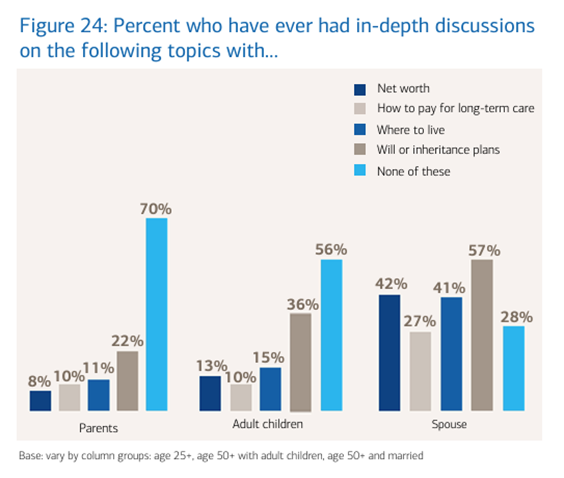

Communication & transparency: Open discussions about the intentions and expectation of giving money is critical. Merrill Lynch’s research found that both parents and children are likely to keep their head in the sand.

Both parents and children should share their needs, goals and perspectives. Mutual respect for each other’s views, paired with open communication is key to responsible stewardship.

Getting the balance right

Financial gifts come with risks and have the potential to hinder growth and independence in profoundly negative ways.

For some children, it means they never learn to become financially independent. So, parents need to be aware of what and how they teach children about money from a young age. It should be a process that teaches children about decision-making, risks and problem-solving.

It can also affect a child’s self-esteem and confidence. Many children have a need to make their own way in life and their purpose and self-esteem are linked to their financial successes in life. It is important to recognise your child’s needs and goals and allow them the opportunity to use the funds appropriately. If a parent is very descriptive and authoritarian about how gift money should be used, it may have the opposite effect and put strain on the relationship between parent and child.

Lastly, recipient children should think about “ringfencing” the inheritance to ensure it remains excluded in the case of a divorce. Using inheritance money to fund joint expenses or to pay off joint assets can complicate matters.

Final Thoughts

Reflecting on my life, I see how my parents did everything in their power to put my sister and me first. They still do - my mother will spend her last cent to help us. And while endearing and appreciated, it’s not always the right thing to do.

So, ask yourself this; Am I forgoing my financial independence? Do I want to depend on my children? Am I serving my child?

Consider your own financial position and whether gifting funds to your children makes sense. If it does, have the courage to discuss it openly as a family. These gifts have the potential to enrich both parents and children’s lives. Knowing how to give and accept this gift may be your biggest obstacle but once overcome, and used correctly, it can be a gateway to goodness and joy.

<Foundation Family Wealth is an Authorised Financial Services Provider>