Humans like certainty. In areas we know least, we are more intent on it. We think in right or wrong, yes or no, black or white, despite the whole world being governed by probability. It’s just easier this way. It creates the certainty we crave. It makes the unpredictable, predictable and by doing so reduces anxiety and stress. This is a technique many advisors and market commentators use, sometimes unbeknown to themselves.

But it is a dangerous strategy. It’s impossible to predict the future. Yet, some spend their lives trying to forecast and predict the outcomes of things completely out of their control. Of course, with research we can put a probability on an outcome, but very seldom can we know for sure.

This reminds me of a beautiful old fable about the uncertainty of life. The fable illustrates how important it is not to dwell on things you cannot control.

There was a farmer whose only horse ran away. That evening the neighbours gathered to commiserate with him since this was such bad luck. “Your farm will suffer, and you cannot plow,” they said. “Surely this is a terrible thing to have happened to you.”

He said, “Maybe yes, maybe no.”

The next day the horse returned but brought with it six wild horses, and the neighbours came to congratulate him and exclaim at his good fortune. “You are richer than you were before!” they said. “Surely this has turned out to be a good thing for you, after all.”

He said, “Maybe yes, maybe no.”

The following day, his son tried to saddle and ride one of the wild horses. He was thrown and broke his leg, and he couldn’t work on the farm. Again, the neighbours came to offer their sympathy for the incident. “There is more work than only you can handle, and you may be driven poor,” they said. “Surely this is a terrible misfortune.”

The old farmer said, “Maybe yes, maybe no.”

The day after that, conscription officers came to the village to seize young men for the army, but because of his broken leg, the farmer’s son was rejected. When the neighbours came again, they said, “How fortunate! Things have worked out after all. Most young men never return alive from the war. Surely this is the best of fortunes for you!”

And the old man said again, “Maybe yes, maybe no.”

So, when it comes to your financial planning amidst global pandemics and financial crises, how do you plan for uncertainty?

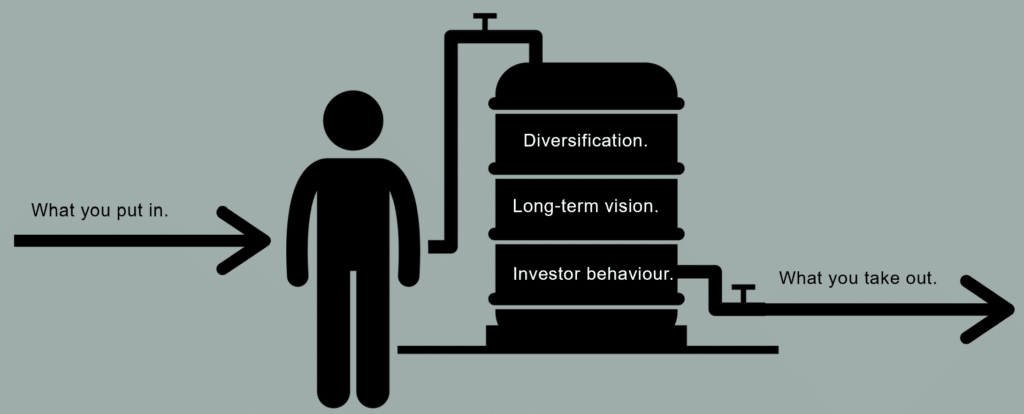

Focus on what you can control

There are 3 things:

- How much you save. The more you save and the earlier you begin saving the more likely you are to withstand any unplanned event.

- How you invest your money.

- Diversify – this is the single most important step you can take to protect yourself against the unknown.

- Take a long-term view.

- Focus on your own behaviour (more about this in the next point).

- How much you spend. Understand your budget well. Know where you can easily cut costs when necessary.

Consider your own behaviour

Be very careful of extreme views. All or nothing outcomes. 0% to 100% shifts in investments or allocations.

Look out for words like: “I’m certain,” “guaranteed,” and “undoubtably the case”.

“History is mostly the study of unprecedented events, ironically used as a map of the future.” Morgan Housel.

We cannot assume that the past will repeat itself. We also cannot assume that if it was true for someone else it will be true for you.

Do scenario analysis (the “what if” test)

During the scenario analysis process, we aim to answer questions like:

- What if my partner dies?

- What if I’m in an accident and I cannot work?

- What if I lose my job or robots take over my profession?

- What impact can returns, and the order in which I get them, have on the longevity of my money?

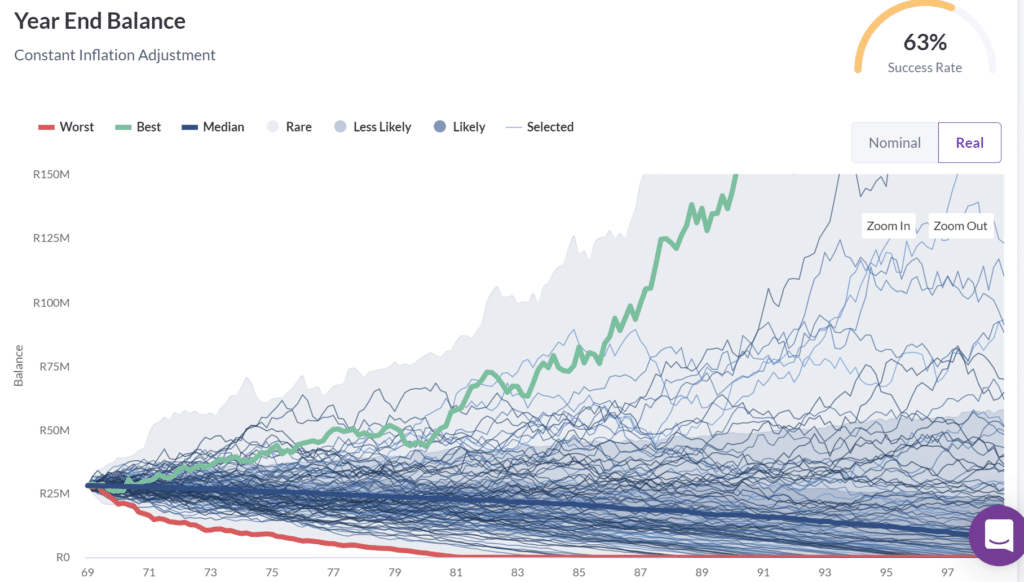

To illustrate what we do for our clients in a scenario analysis, let’s consider the order of returns question.

If we use ordinary financial projections, and assume returns come in a straight line (9% per annum), you can easily calculate whether a client’s money will last his/her lifetime. And very often these type of calculations will indicate that clients are on track for their money to last their lifetime given their expenses. The problem is that returns DON’T come in a straight line. They move in ebbs and flow. So, the order of returns can create havoc with projections. Thus, how would you know if your plan is still on track?

There are some fantastic tools we use to test how robust your retirement plan is. We can simulate hundreds or possible outcomes and run your plan against each scenario to see if your money is still likely to last your lifetime.

In the example above our client will stay on track 63 out of every 100 possible scenarios. Said another way, there is a 63% probability that his/her money will last his/her lifetime, regardless of what market returns are.

A test like this gives richness and context to a complex question like, “will my money last?”

Get help

According to Nobel-winner Daniel Kahneman it’s easier to recognise someone else’s errors rather than your own. At Foundation Family Wealth we believe that good advice significantly increases the likelihood of success.

There are many studies across the world that show the value and importance of an ongoing advice relationship. Vanguard has on of the world’s longest running studies. They estimate that advisors can add over 3% per annum (in USD) to returns for their clients. Their study also makes the point that the most significant opportunities for an advisor to add value do not present themselves every year, hence the importance of an ongoing relationship.

At Foundation Family Wealth, not only can we help you think about the ‘maybe yes’ and ‘maybe no’ scenarios and the impact it will have on your life, but we also monitor this on an ongoing basis. Our best client relationships are those where we work with clients to answer the ‘what if’ questions. A good advisory relationship is not that of a passive participant being lectured by an expert, but is an active co-labouring to find answers. Although we have expertise, we are not the experts on our clients’ lives and their ‘what ifs’.

This year has taught me many things, but I’m especially grateful for another opportunity to learn how to live with uncertainty. As uncomfortable as it is, it’s much less dangerous than trying to find certainty where there is none.