Money has power.

Money can only hold as much power as we give it and as humans, we have given it immense power. Everyone is interested in money, and almost all of us feel worried, or even fearful that there will never be enough. No one escapes the power of the push and pull of money.

One of the reasons money is so powerful is because of what it represents in our lives. So much of our self-worth, success and sense of achievement is in response to money. This is ingrained in us from a young age as we see the power that money has in our family and community. We can see who earns it and who doesn’t. We can see what our parents are willing to do to acquire money and we can see the things it buys. We are born into a culture of money.

In such a culture, where our relationship with money influences our self-worth, what happens if you suddenly get gifted a lot of money? You did not work for or earn this money, so what does it say about you? For many, this seems to create a deeply conflicted relationship with the money. Inheriting wealth triggers a series of complex emotions, and it shows up differently for everyone. For some there is a sense of entitlement, and for others a feeling of “I don’t deserve it”.

Families with multi-generational wealth may be less affected by these issues because children are often exposed to the wealth or family business from a young age. Their identity in many ways already attached to the wealth.

In this article, we focus on the guilt that arise for those feeling undeserving. However it shows up, not being able to deal with these complexities poses its own risks as it can lead to making poor decisions about the money. This can have a devastating effect on their financial well-being.

Understanding guilt.

Research from Ascent Private Capital Management of U.S. Bank shows us that guilt is mostly triggered by our fears regarding lack of acceptance.

The research states that “guilt likely exists as a mechanism to help us recognize when we’ve done something that hurts our social standing within a group. It makes us want to maintain our standing and acceptance within the group and helps us realize that we need to engage in reparative acts. Guilt is the perception that what we did, or what was done to us, such as receiving wealth, is having a negative impact and affects our social bonds.”

In other words, a person who inherits money often feels guilty because the inherited money hurts how they fit into their social group, into their life. Here, the power of money is that it ostensibly changes that person’s identity and this can have a negative impact as it threatens that person’s sense of belonging.

Consider this example: Naeema is the only daughter of immigrants from India. Her parents worked selflessly for many years in the textile industry. They built a very successful business, but despite their success, they lived humble lives and rarely enjoyed their money. Naeema inherited her parent’s sizeable wealth. Yet, she feels guilty. Naeema is worried that because of the inherited wealth, people may now see her differently; she worries that she will no longer have the easy acceptance within her social group that she had before. Already their comments that it is silly to feel guilty about the money positions her further outside the group than before. The guilt not only isolates her but also paralyses her with regard to making any financial decisions about the money. She gets stuck.

Dealing with guilt.

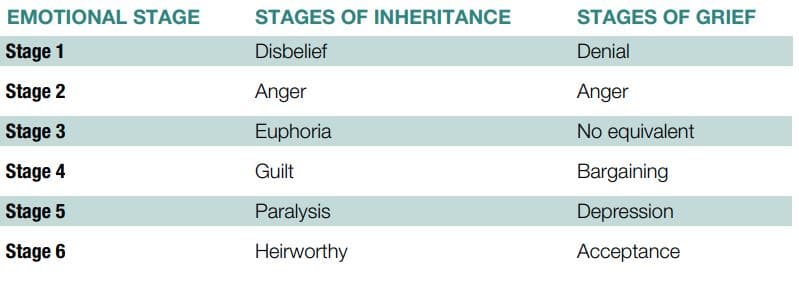

Ascent Private Capital Management of U.S. Bank’s researchers realised that how you deal with your inheritance is very closely linked to dealing with the grief of losing someone. These are typically the stages you may experience:

Source: Ascent Private Capital Management of U.S. Bank

Learning to deal with inherited wealth is a process like grief is. It is a process that takes you through various emotional stages.

Stage 1:

The emotional stages of inheritance start with shock or disbelief at what is happening.

Stage 2:

Anger sets in. This may be at the death itself and the circumstances surrounding it.

Stage 3:

In this stage, a feeling of freedom or relief is experienced in light of what the money may offer. Some heirs never move past this stage. If this happens heirs tend to spend the money very quickly – a bit like people winning the lotto.

Stage 4:

Here, a feeling of guilt starts to grow. This stage can be exacerbated when the death was of a loved one – something difficult to process in itself. So when overwhelmed by the guilt that inheritance can trigger (specifically the complex issues around a person’s sense of belonging and identity) it becomes an especially difficult stage. It is important to understand that this is a very natural stage.

Stage 5:

Moving past the stage of guilt is crucial because if you get stuck in the guilt stage it leads to paralysis, avoidance or an inability to make any decisions.

The paralysis stage can be prolonged by various factors. One is that the money inherited serves as a constant reminder of the person lost. A client recalled transferring money one day and thinking, “Oh yeah, Dad died”. He told me that this feeling made him avoid making money decisions at all costs.

Another client told me that she didn’t want to squander her mother’s hard-earned savings; the fear of not honouring her mother properly left her in a state of paralysis.

Stage 6:

Ultimately the heir comes to terms with reality and the inheritance. This stage is called becoming “heir worthy”. It may take time, but it’s important to move through all the stages to get to this point.

Financial planning and inheritance.

As financial planners, we often see clients as they move from paralysis to the final stage. This is when they are ready to make decisions about their future and the role the money can play. The feeling of guilt can be very overwhelming for some, and to get to this point can take years. This can lead to capital destruction and we, therefore, encourage heirs to get the help they need as soon as they can.

Let’s expand on some of the most important factors to consider when doing your financial planning after receiving an inheritance.

Never make decisions in a rush.

Don’t rush to make big decisions considering the difficult emotions you are working through. You don’t have to decide today. If however, you don’t feel ready at least make sure the money is held in an interest-bearing money market account to insure you earn interest whilst pausing.

Letting go of past money messages.

Naeema’s story speaks about her humble, hardworking parents that always worried about money. In many ways, their frugality ensured their success. Naeema struggles with the same worry about money that they had – whether there will be enough. It is difficult for her to spend money on luxuries or things she enjoys doing. In her case, the worry is completely unfounded because her parents left her with a small fortune.

We all grow up with money messages from our parents. It shapes the way we think about money and our futures. Some money messages can serve us well, but some can hold us back from living a happy, meaningful life, like in Naeema’s case. We need to identify those messages and practice letting go of any that have a negative impact. Doing so will help us move forward.

What are your needs?

When past money messages drive our decision making, we often forget about our own needs and passions in life. The reality is that the money no longer belongs to someone else. It now belongs to you and can serve your needs. It is therefore important to establish exactly what your needs, passions and future aspirations are.

Naeema has been working in her parent’s textile business for as long as she can remember. She feels a responsibility to keep the family business going but it has never been her own passion. If she decides to keep the family business going, she is doing it because she doesn’t want to let her parents down and because she wants to uphold what was important to them. Naeema does however have another choice. She can approach the money with the same spirit in which her parents lived their life. But not within the same field. She can apply it to her own life and passions.

Naeema dreams of starting her own catering business. If she applies the same work ethic and humbleness she observed and learnt from her parents to her own business, she will still be honouring her parents. And her own needs.

To enjoy the true opportunity and freedom inherited wealth brings it is crucial to understand what your own needs and passions are. Only then can you apply the money in a way the serves your needs without the guilt.

Get professional help.

These are the most important specialists that you may need to involve when making your financial plans.

Fiduciary and estate specialist – Winding up an estate can be traumatising, time-consuming and complex. It’s worthwhile appointing an executor with the necessary skill and experience to get through the process quickly and efficiently.

If a trust is involved it can be invaluable having a professional trustee to guide and support you. Most importantly the professional trustee will ensure that the trust complies with all regulations.

Tax consultant – Death triggers taxes, and it’s important to ensure that these costs are kept at a minimum. Tax consultants can also help with other complexities such as dealing with the Reserve Bank if inherited wealth is held offshore.

Financial planner – Financial planners help heirs to define their needs and goals. They use scenario planning to illustrate what is possible. At Foundation we stress test the scenarios against various possible obstacles to ensure your success. A financial planner can recommend suitable investments to help you achieve your long-term goals. It’s also important to monitor and adjust your financial plan on an ongoing basis to ensure that you stay on track.

Talk about the money.

It can be very distressing when you have to deal with sudden wealth, especially if you are unfamiliar with investments, financial markets or making any financial decisions. We often see this with widows who left all the financial decisions to their late husbands.

At Foundation we encourage couples and families with generational wealth to have open discussions about the money. We even facilitate conversations for families that struggle to talk about money. If you are the financial decision-maker, include the heirs in your financial planning discussions.

When heirs are involved with the money before inheriting it, they often have a better understanding of what the benefactor’s intentions were, and it’s, therefore, easier for them to make decisions about the money. They also tend to take ownership of the money in more confidently and comfortably.

Honour.

When reality sets in and you take responsibility for the money, it can be very empowering. An important part of taking responsibility is accepting that the money is now yours. This is an important distinction that must be made in order to move forward. Accepting that the money is yours will help you apply the money to your own needs and future goals. If you don’t take responsibility for the money as your own, you will struggle with guilt as you will always feel like you are spending money that is not yours. Get help to work through the guilt if you need to.

If it’s important for you to honour the benefactor, choose to use the money in a way that honours the spirit with which they lived. If they were generous, be generous; if they were humble, be humble; if they ensured that elderly family members were looked after, look after them; if they enjoyed a once-a-year splurge, enjoy a once-a-year splurge. But do it in your way and on your own terms.

An inheritance is a beautiful gift. It is kind. It is generous. It’s for the benefit of your family. But most importantly, it is yours. You can control the power money has if you have confidence in your ability to choose the direction you want to go and then plan for it.